The 50/30/20 Rule: A Simple Guide to Budgeting Your Money

Have you ever stared at your bank account at the end of the month, wondering where all your money disappeared? That sinking feeling when you realize you’ve spent your entire paycheck without anything to show for it except a collection of receipts and a growing sense of financial anxiety. You’re not alone in this struggle – millions of people feel overwhelmed by the complexities of managing money, drowning in spreadsheets, budgeting apps, and conflicting financial advice.

But what if there was a beautifully simple solution that could transform your financial chaos into clarity? What if you could finally take control of your money without needing an accounting degree or spending hours each week tracking every penny? The answer lies in understanding and implementing the 50/30/20 rule – a straightforward budgeting method that has helped countless beginners build financial stability and peace of mind.

Your journey toward financial freedom doesn’t have to be complicated. Today, you’ll discover how this simple percentage-based approach can revolutionize your relationship with money, reduce your stress, and set you on the path to achieving your dreams.

Understanding the 50/30/20 Rule: Your Foundation for Financial Success

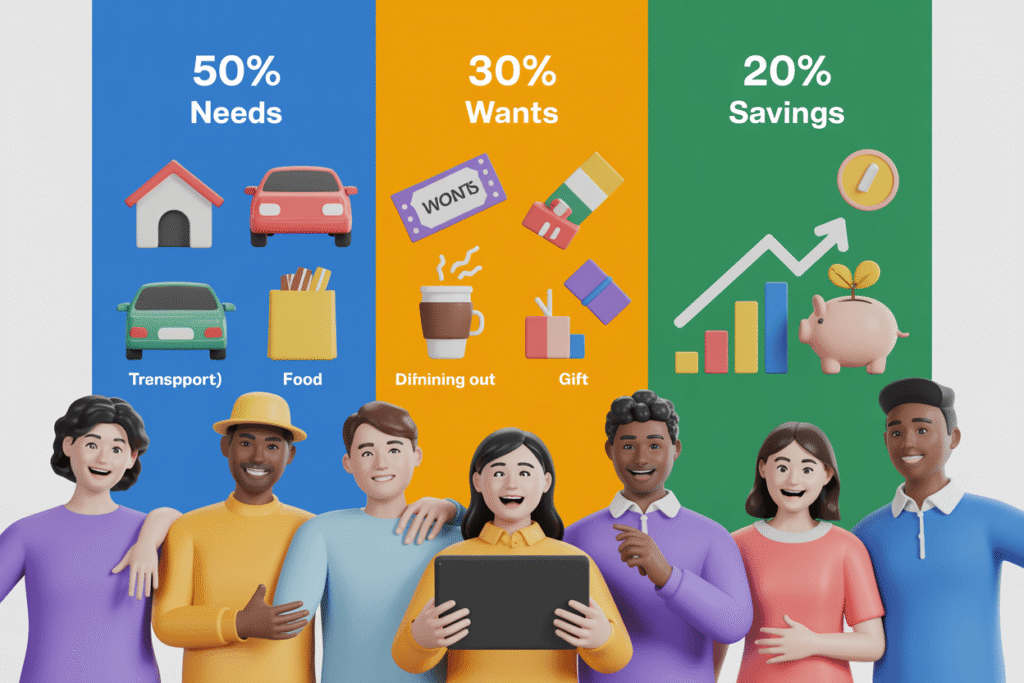

50/30/20 Rule Calculator

Simplify your budgeting process by seeing your ideal income split.

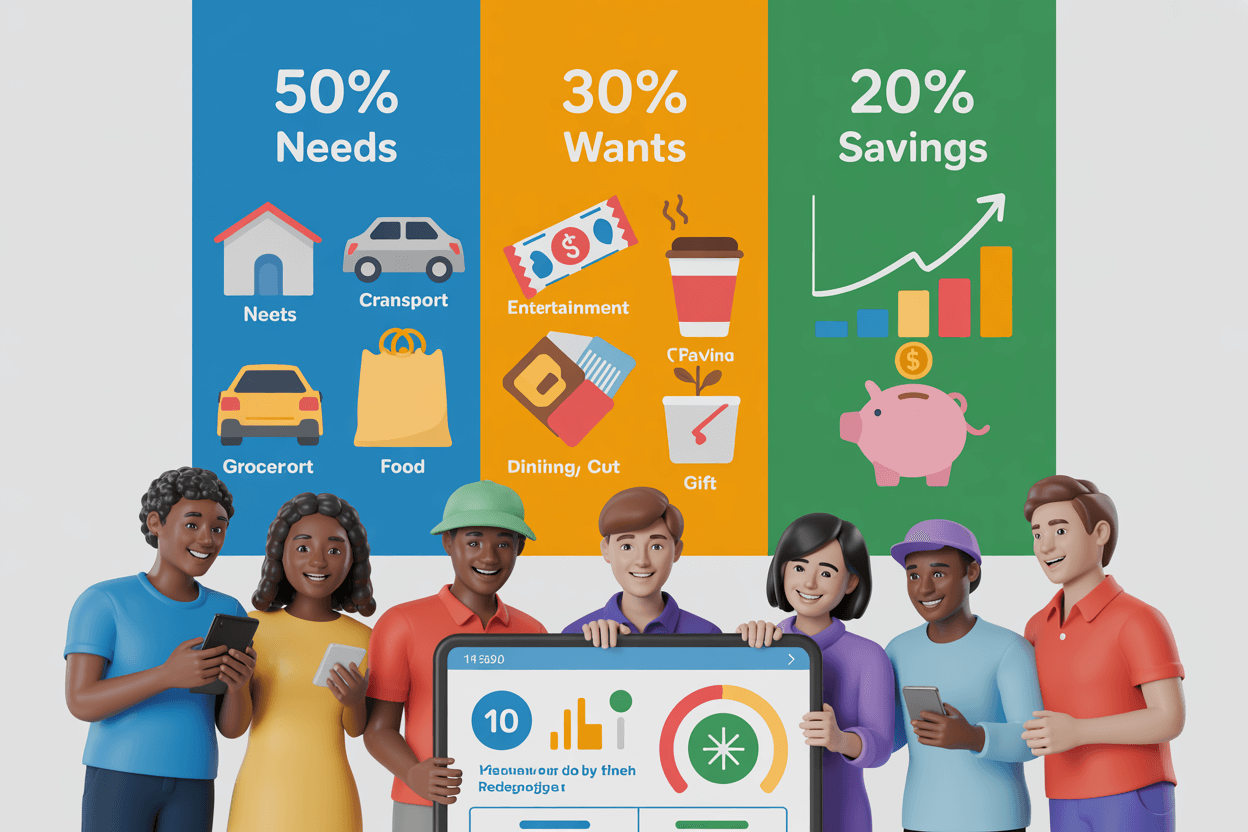

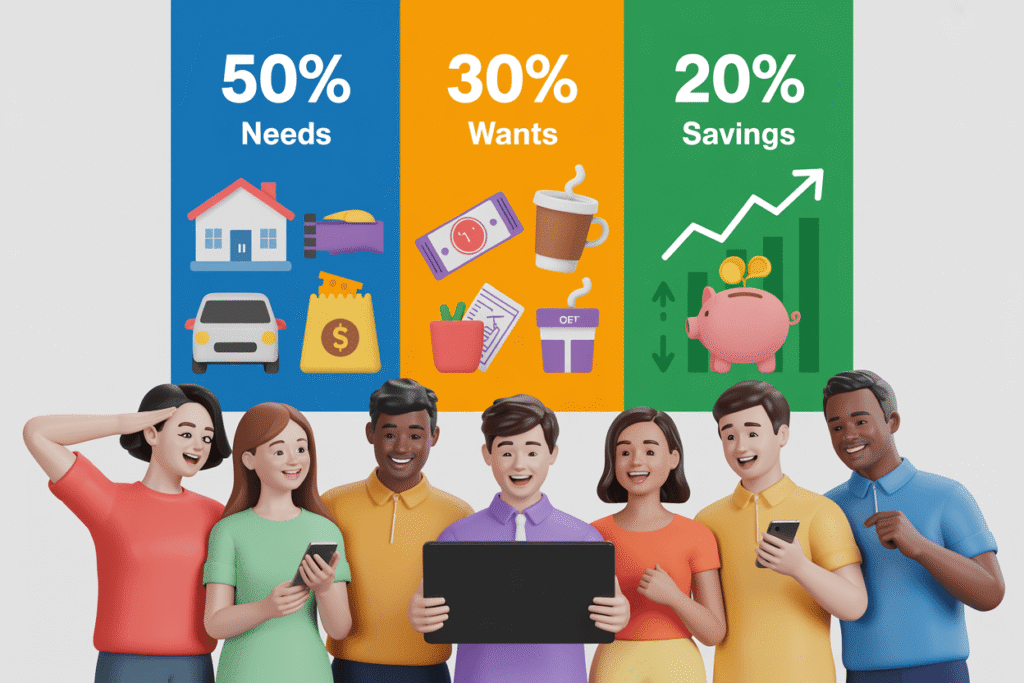

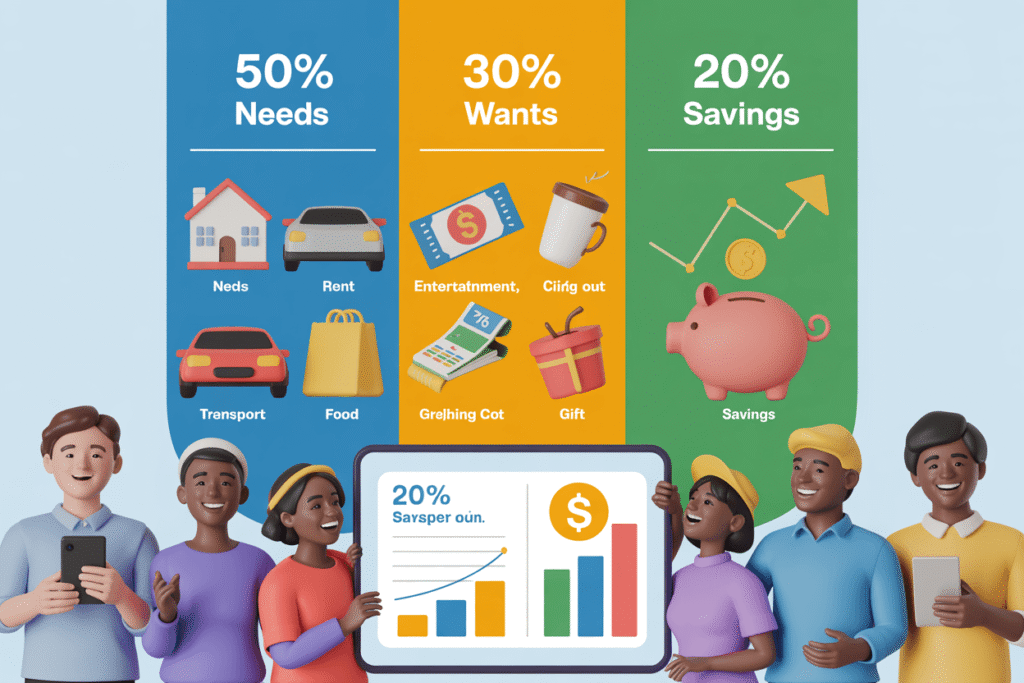

Essential Needs (50%)

Housing, Groceries, Bills, Transport

Personal Wants (30%)

Dining, Hobbies, Subscriptions, Fun

Savings & Debt (20%)

Emergency Fund, Investing, Extra Debt

Ready to Start Budgeting?

Download our “Simple 50/30/20 Budgeting Checklist” to categorize your expenses correctly and stay on track.

What Is the 50/30/20 Budgeting Method?

The 50/30/20 rule represents one of the most accessible budgeting frameworks ever created. This method divides your after-tax income into three distinct categories, each serving a specific purpose in your financial ecosystem.

The Three Categories Breakdown:

- 50% for Needs: Essential expenses that keep your life functioning

- 30% for Wants: Discretionary spending that brings joy and fulfillment

- 20% for Savings and Debt Repayment: Building your financial future

The brilliance of this system lies in its simplicity. Instead of tracking dozens of spending categories, you focus on three fundamental buckets that encompass your entire financial life.

The Origins and Psychology Behind the 50/30/20 Rule

This budgeting method gained widespread recognition through Senator Elizabeth Warren’s book “All Your Worth,” where she advocated for balanced money management that doesn’t sacrifice quality of life for financial responsibility.

Why This Method Works Psychologically:

- Reduces decision fatigue by simplifying complex financial choices

- Provides clear boundaries without feeling overly restrictive

- Balances present enjoyment with future security

- Creates sustainable habits through manageable percentages

- Eliminates guilt around discretionary spending within limits

Love financial peace of mind? Check out these top budgeting methods and get inspired to share your own financial game plan!

How to Create a Bi-Weekly Budget That Actually Works (Perfect If You Get Paid Every Two Weeks)

7 Best Budgeting Apps of 2024 to Take Control of Your Money

The 50/30/20 Rule: Master Your Money with This Simple Budgeting Method for Beginners

How to Create a Zero-Based Budget That Actually Works

Zero-Based Budgeting: Transform Your Finances with a Budget That Actually Works in 2025

Breaking Down the 50/30/20 Rule Categories: Where Your Money Should Go

The 50% Needs Category: Essential Living Expenses

Your needs category represents the foundation of your financial survival. These expenses would continue even if you lost your job tomorrow and needed to maintain basic living standards.

What Qualifies as Needs:

- Housing costs: Rent, mortgage payments, property taxes, essential utilities

- Transportation: Car payments, gas, public transit, necessary vehicle maintenance

- Food basics: Groceries for home cooking, essential meal planning

- Insurance premiums: Health, auto, renters/homeowners insurance

- Minimum debt payments: Credit cards, student loans, other required payments

- Essential utilities: Electricity, water, heat, basic internet service

- Basic clothing: Work attire and necessary replacements

What Doesn’t Qualify as Needs:

- Premium cable packages or streaming services beyond basic needs

- Dining out frequently or gourmet grocery items

- Luxury car payments or premium insurance coverage

- Designer clothing or frequent shopping sprees

- High-end gym memberships or personal training

The 30% Wants Category: Enjoying Life Within Limits

Your wants category gives you permission to enjoy life while maintaining financial responsibility. This allocation ensures you don’t feel deprived while working toward your financial goals.

Typical Want Category Expenses:

- Entertainment: Movies, concerts, streaming services, hobbies

- Dining experiences: Restaurants, takeout, specialty coffee

- Travel and vacations: Weekend trips, vacation funds, travel experiences

- Premium upgrades: Better phone plans, premium subscriptions

- Fitness and wellness: Gym memberships, spa treatments, fitness classes

- Social activities: Drinks with friends, date nights, recreational activities

- Personal interests: Books, games, craft supplies, sporting equipment

The 20% Savings and Debt Repayment: Building Your Future

This category represents your commitment to financial security and freedom. Every dollar allocated here works toward improving your future financial position.

Priority Order for Your 20%:

- Emergency fund: Build 3-6 months of expenses for unexpected situations

- High-interest debt: Pay off credit cards and loans above 7% interest

- Retirement savings: 401(k) contributions, especially with employer matching

- Medium-term goals: House down payment, car replacement fund

- Long-term investments: Index funds, stocks, additional retirement accounts

Implementing the 50/30/20 Rule: Step-by-Step Budgeting Guide

Calculating Your 50/30/20 Budget Breakdown

Step 1: Determine Your After-Tax Income Start with your monthly take-home pay after taxes, insurance deductions, and other automatic withdrawals.

Step 2: Calculate Your Category Amounts

| Monthly Income | Needs (50%) | Wants (30%) | Savings/Debt (20%) |

|---|---|---|---|

| $3,000 | $1,500 | $900 | $600 |

| $4,000 | $2,000 | $1,200 | $800 |

| $5,000 | $2,500 | $1,500 | $1,000 |

| $6,000 | $3,000 | $1,800 | $1,200 |

| $8,000 | $4,000 | $2,400 | $1,600 |

Step 3: Track Your Current Spending Review three months of expenses to understand your current spending patterns across all categories.

Setting Up Your 50/30/20 Budget System

Choose Your Tracking Method:

Option 1: Multiple Bank Accounts

- Direct deposit splits paycheck automatically

- Separate accounts for needs, wants, and savings

- Prevents overspending through account limits

Option 2: Budgeting Apps

- YNAB (You Need A Budget) for detailed tracking

- Mint for automatic categorization

- Personal Capital for investment tracking

- Simple spreadsheet solutions

Option 3: Cash Envelope System

- Physical cash for discretionary spending

- Automatic transfers for fixed expenses

- Visual spending limits prevent overspending

Monthly Budget Review and Adjustment Process

Weekly Check-ins (15 minutes):

- Review spending in each category

- Identify any overspending early

- Adjust remaining week’s plans accordingly

Monthly Deep Dive (45 minutes):

- Calculate actual percentages versus targets

- Analyze spending patterns and trends

- Adjust categories for upcoming month’s changes

- Celebrate successes and identify improvement areas

Common Challenges with the 50/30/20 Rule and Solutions

When Your Needs Exceed 50% of Income

High Cost of Living Areas: If housing costs alone consume 40% of your income, you’ll need to make strategic adjustments.

Solutions for Needs Overspending:

- Housing adjustments: Consider roommates, smaller spaces, or relocation

- Transportation alternatives: Public transit, carpooling, or moving closer to work

- Insurance shopping: Compare rates annually for better deals

- Utility optimization: Energy-efficient practices and plan comparisons

- Food strategies: Meal planning, bulk buying, and cooking at home

Modified Ratios for High-Cost Situations:

- 60/25/15 temporarily while addressing high expenses

- 55/25/20 as a compromise position

- Focus on increasing income rather than just cutting expenses

Managing Irregular Income with the 50/30/20 Rule

Strategies for Freelancers and Gig Workers:

Base Budget on Lowest Monthly Income:

- Calculate your worst-case monthly earnings

- Build budget categories around this minimum

- Treat additional income as bonus for extra savings

Create Income Smoothing Fund:

- Save high-earning months’ excess in a buffer account

- Use buffer during low-earning periods

- Maintain consistent monthly spending regardless of income fluctuations

Percentage-Based Approach:

- Apply 50/30/20 to whatever you earn each month

- Adjust dollar amounts while maintaining percentages

- Build larger emergency fund for income volatility

Advanced 50/30/20 Rule Strategies for Long-Term Success

Optimizing Each Category for Maximum Impact

Needs Category Optimization:

- Housing hacks: House sitting, rental arbitrage, or strategic roommate selection

- Transportation efficiency: Car sharing programs or strategic public transit use

- Food cost reduction: Meal planning, bulk buying, and seasonal eating

- Insurance bundling: Multi-policy discounts and annual payment savings

- Utility management: Time-of-use rates and energy efficiency investments

Wants Category Enhancement:

- Experience over things: Prioritize memories and personal growth

- Social cost sharing: Group activities and potluck-style gatherings

- Seasonal adjustments: Budget more for summer activities, less for winter months

- Quality over quantity: Choose fewer, higher-quality discretionary purchases

Savings Category Acceleration:

- Employer match maximization: Never leave free money on the table

- Tax-advantaged accounts: HSAs, 401(k)s, and IRAs for tax benefits

- Automatic increases: Annual percentage point increases in savings rate

- Windfall allocation: Direct bonuses and tax refunds to this category

Adapting the 50/30/20 Rule Through Life Stages

Early Career Modifications (20s-30s):

- Higher wants percentage for social activities and experiences

- Focus emergency fund building before aggressive investing

- Consider 45/35/20 split for social and career development

Family Building Phase (30s-40s):

- Adjust needs category for childcare and family expenses

- Reduce wants percentage temporarily for family priorities

- Possible 55/25/20 split during expensive family years

Pre-Retirement Optimization (50s-60s):

- Increase savings percentage to 25-30% for retirement acceleration

- Reduce wants spending as lifestyle stabilizes

- Consider 50/25/25 or 45/25/30 splits for retirement preparation

Technology Tools and Apps for 50/30/20 Budgeting

H3: Best Budgeting Apps for the 50/30/20 Method

Comprehensive Budgeting Solutions:

| App Name | Cost | Key Features | Best For |

|---|---|---|---|

| YNAB | $14/month | Zero-based budgeting, goal tracking | Detailed planners |

| Mint | Free | Automatic categorization, credit monitoring | Set-and-forget users |

| Personal Capital | Free | Investment tracking, net worth monitoring | Investment-focused |

| PocketGuard | Free/$7.99/month | Simple 50/30/20 setup, spending alerts | Beginners |

| Goodbudget | Free/$10/month | Envelope budgeting, family sharing | Cash-based budgeters |

Automation Features to Look For:

- Automatic categorization of expenses

- Bill reminder notifications to avoid late fees

- Savings goal tracking with visual progress

- Spending limit alerts before category overspending

- Monthly report generation for budget reviews

DIY Spreadsheet Solutions for 50/30/20 Budgeting

Essential Spreadsheet Components:

Income Tracking Section:

- Monthly take-home pay calculation

- Side income and irregular earnings

- Annual income projections

Category Breakdown Calculator:

- Automatic percentage calculations

- Dollar amount allocations

- Comparison to actual spending

Monthly Tracking Tables:

- Daily expense entries

- Category running totals

- Remaining budget displays

Annual Overview Dashboard:

- Month-by-month category performance

- Savings rate progression

- Goal achievement tracking

Measuring Success with the 50/30/20 Rule

Key Performance Indicators for Budget Success

Monthly Success Metrics:

- Category adherence percentage: How often you stay within limits

- Savings rate consistency: Maintaining 20% allocation monthly

- Needs category efficiency: Keeping essential expenses under 50%

- Emergency fund growth: Building toward 3-6 month expense goal

Quarterly Progress Reviews:

- Net worth calculation and quarterly growth

- Debt reduction progress and payoff timeline updates

- Goal achievement assessment for both short and long-term objectives

- Budget ratio effectiveness and adjustment needs

Annual Financial Health Check:

- Overall savings rate including employer contributions

- Investment performance and portfolio diversification

- Insurance coverage adequacy and cost optimization

- Tax efficiency and retirement contribution maximization

Troubleshooting Common 50/30/20 Rule Problems

Problem: Constantly Overspending in Wants Category

Solutions:

- Implement weekly wants spending limits

- Use cash-only policy for discretionary expenses

- Create 24-hour waiting periods for non-essential purchases

- Find free or low-cost alternatives for expensive wants

Problem: Unable to Save 20% Consistently

Root Cause Analysis:

- Income insufficient for current lifestyle

- Hidden expenses classified incorrectly

- Irregular expenses not properly budgeted

- Lack of motivation or clear financial goals

Improvement Strategies:

- Start with 10% savings rate and increase by 2% every six months

- Automate savings transfers immediately after paycheck

- Create specific, motivating financial goals with deadlines

- Track net worth monthly to see progress visually

Beyond the Basics: Advanced 50/30/20 Rule Modifications

The 50/30/20 Rule for High Earners

When Standard Percentages Don’t Apply:

High-income earners often find their needs percentage naturally decreases as income increases. A person earning $200,000 annually doesn’t need twice the housing of someone earning $100,000.

Modified Ratios for High Earners:

- 40/30/30: Increased savings rate for accelerated wealth building

- 45/25/30: Balanced approach with higher savings emphasis

- 40/35/25: Lifestyle inflation allowance with solid savings

Tax Considerations for High Earners:

- Maximize pre-tax retirement contributions

- Consider backdoor Roth IRA strategies

- Implement tax-loss harvesting in investment accounts

- Utilize HSAs for triple tax advantages

The 50/30/20 Rule During Financial Emergencies

Emergency Modifications:

Job Loss Scenario:

- Shift to survival mode: 80/10/10 (needs/wants/savings)

- Pause all debt payments except minimums

- Access emergency fund strategically

- Focus on essential needs only until employment resumes

Medical Emergency Adjustments:

- Redirect wants category to medical expenses

- Negotiate payment plans for large medical bills

- Research assistance programs and insurance coverage

- Maintain minimum savings for ongoing emergencies

Economic Recession Planning:

- Build larger emergency fund (6-12 months expenses)

- Reduce wants spending proactively

- Focus on recession-proof skill development

- Consider side income diversification

Real-Life 50/30/20 Rule Success Stories and Case Studies

Case Study 1: Sarah’s Student Debt Elimination Journey

Starting Situation:

- Monthly income: $4,200 after taxes

- Student loan debt: $45,000 at 6.5% interest

- Credit card debt: $8,000 at 18% interest

- No emergency savings

50/30/20 Implementation:

- Needs (50%): $2,100 for rent, utilities, transportation, minimum payments

- Wants (30%): $1,260 for dining out, entertainment, personal care

- Savings/Debt (20%): $840 split between emergency fund and extra debt payments

Results After 18 Months:

- Emergency fund: $6,000 (3-month safety net)

- Credit card debt: Completely eliminated

- Student loans: Reduced to $38,000

- Improved credit score: Increased by 85 points

Case Study 2: Marcus and Elena’s First Home Purchase

Dual-Income Household Challenge:

- Combined monthly income: $7,800 after taxes

- Goal: Save $60,000 for house down payment in 3 years

- Current rent: $2,000 monthly

- Various consumer debts totaling $15,000

Strategic 50/30/20 Modification:

- Temporarily adopted 50/20/30 ratio

- Redirected extra 10% from wants to house savings fund

- Maintained emergency fund while aggressively saving

Three-Year Results:

- House down payment fund: $62,000

- Consumer debt: Eliminated completely

- Emergency fund: $23,400 (3-month expenses)

- Successfully purchased $280,000 home

Frequently Asked Questions About the 50/30/20 Rule

Is the 50/30/20 rule realistic for low-income earners?

The 50/30/20 rule can be challenging for very low incomes where basic needs consume most earnings. Start with any savings percentage possible, even 5%, and gradually increase as income grows. Focus on increasing income through skills development while maintaining the percentage concept.

How do you apply the 50/30/20 rule with irregular income?

Base your budget on your lowest monthly income over the past year. Apply the 50/30/20 percentages to this amount. During higher-earning months, direct excess income to boost your savings category or build an income-smoothing fund.

What happens if I can’t stick to the 50/30/20 rule perfectly?

Perfection isn’t the goal – progress is. If you overspend in one category, adjust the others accordingly or aim for weekly balance rather than daily precision. The rule provides structure, not rigid restrictions.

Should debt payments count as needs or savings in the 50/30/20 rule?

Minimum debt payments belong in the needs category since they’re required expenses. Extra debt payments above minimums should come from your savings/debt repayment (20%) category, as they improve your financial position.

How often should I review and adjust my 50/30/20 budget?

Review your budget monthly to track performance and make small adjustments. Conduct deeper reviews quarterly to assess whether the percentage splits still work for your situation. Annual reviews help align your budget with major life changes.

Can I modify the 50/30/20 rule percentages for my situation?

Absolutely! The 50/30/20 rule provides a starting framework. Common modifications include 60/20/20 for high-cost areas or 40/30/30 for high earners focused on accelerated savings. The key is maintaining balance between current needs and future security.

Conclusion: Your Path to Financial Freedom Through the 50/30/20 Rule

The journey from financial chaos to clarity doesn’t happen overnight, but the 50/30/20 rule provides the roadmap you need to navigate toward lasting financial success. This simple yet powerful framework eliminates the overwhelm of complex budgeting systems while ensuring you address every aspect of your financial life – from today’s necessities to tomorrow’s dreams.

Remember, the magic of this budgeting method lies not in its mathematical precision, but in its psychological wisdom. By giving yourself permission to spend on wants while mandating savings for your future, you create a sustainable approach that grows with you through every life stage and income level.

Your financial transformation begins with a single decision to take control. Whether you’re drowning in debt, living paycheck to paycheck, or simply seeking better money management, the 50/30/20 rule offers the structure you need without sacrificing the flexibility you want.

The path forward is clear: calculate your numbers, set up your systems, and begin tracking your progress. Every month you successfully implement this rule brings you closer to financial freedom, reduced money stress, and the confidence that comes from knowing you’re building a secure future while still enjoying life today.

Ready to transform your financial life? Take these action steps this week:

- Calculate your 50/30/20 breakdown using your current take-home income

- Review three months of expenses to understand your current spending patterns

- Choose your tracking method – whether apps, spreadsheets, or bank account separation

- Set up automatic transfers for your savings and debt repayment category

- Schedule monthly budget review sessions to stay on track and make adjustments

Your future financial security starts with today’s decision to take control. The 50/30/20 rule isn’t just about managing money – it’s about designing a life where financial stress no longer holds you back from pursuing your dreams and living with confidence.