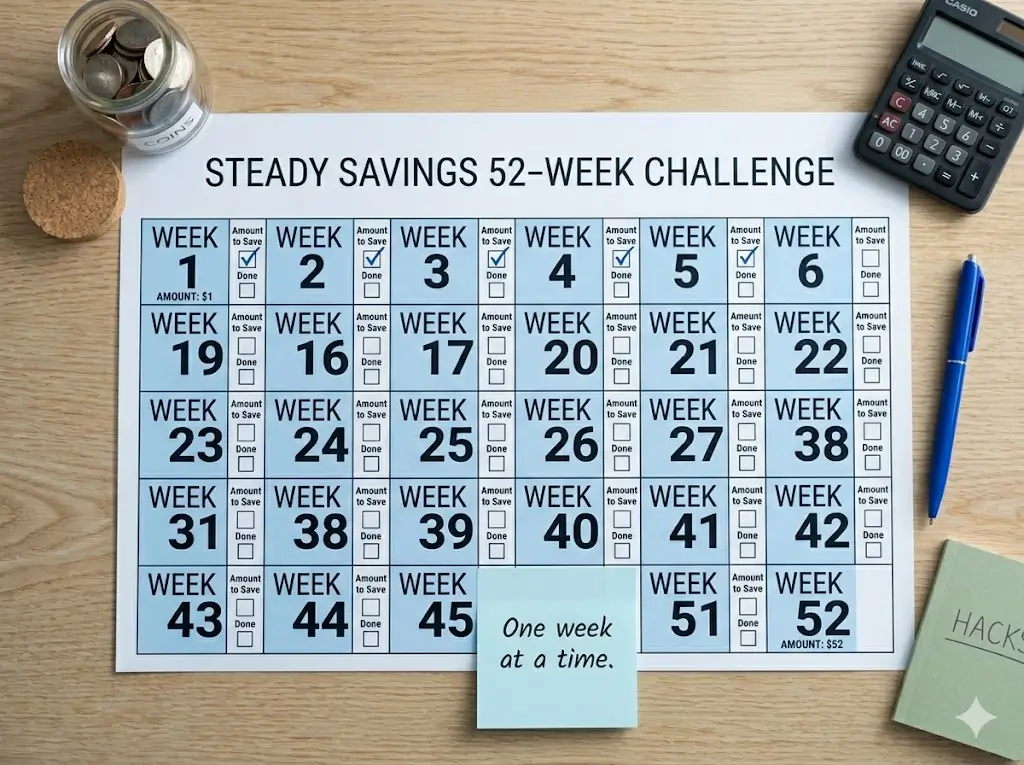

The Ultimate 52 Week Money Saving Challenge to Fund Your Side Hustle

Did you know that 67% of online entrepreneurs fail before making their first dollar simply because they run out of initial startup capital? It’s a harsh reality: while starting a work from home business is cheaper than ever, it still requires some financial runway to cover software, hosting, or initial ad spend.

If you are eager to build passive income but have zero room in your current budget, the 52 Week Money Saving Challenge is the exact framework you need. By gamifying your personal finances, this challenge helps you effortlessly accumulate $1,378 over a year—without feeling deprived.

Think of this not just as a savings plan, but as your first true monetization strategy. By optimizing your personal profit margins and retaining the cash you already make, you are effectively generating tax-free revenue. Let’s dive into how you can use this systematic challenge to fund your future financial freedom.

What You’ll Need to Get Started

How much could YOU save in 52 weeks?

Customize your weekly savings challenge below to reveal your personalized 1-year potential.

How much extra will you add each week? (Standard is $1)

Any extra flat amount you can save each week? (e.g. skipping a $5 coffee)

You do not need an accounting degree or expensive financial software to start building your digital income seed fund. This challenge is designed for absolute beginners and requires minimal setup.

- A Dedicated “Capital” Account: A free, High-Yield Savings Account (HYSA) separate from your daily checking account.

- Visual Tracking Tool: A printable 52-week checklist or a simple Google Sheets template.

- Initial Investment: $1. Literally, you only need one single dollar to start week one.

- Skill Requirements: Basic consistency, the ability to set up automatic bank transfers, and a commitment to delayed gratification.

- Free Alternatives: Instead of paying for a premium budgeting app like YNAB, use the free version of EveryDollar or a customized Excel spreadsheet.

Love financial peace of mind? Check out these top budgeting methods and get inspired to share your own financial game plan!

How to Create a Bi-Weekly Budget That Actually Works (Perfect If You Get Paid Every Two Weeks)

7 Best Budgeting Apps of 2024 to Take Control of Your Money

The 50/30/20 Rule: Master Your Money with This Simple Budgeting Method for Beginners

How to Create a Zero-Based Budget That Actually Works

Zero-Based Budgeting: Transform Your Finances with a Budget That Actually Works in 2025

Time Investment

Unlike building complex revenue streams from scratch, the 52 Week Money Saving Challenge offers a guaranteed return on a surprisingly minimal time investment.

- Setup Time Required: 15 to 20 minutes to open a separate savings account and print your tracking sheet.

- Daily/Weekly Time Commitment: 5 minutes per week to physically (or digitally) transfer the funds and check off your progress.

- Timeline to First Results: Immediate. You establish a winning psychological habit the moment you deposit your first dollar.

- Realistic Expectations: Most beginners see a profound shift in their spending mindset within 60-90 days of consistent effort, making it easier to naturally cut back on variable expenses.

Step-by-Step Implementation Guide

Follow these actionable steps to execute the 52 Week Money Saving Challenge successfully and build your side hustle capital.

Step 1: Understand the Core Mathematics

The premise is beautifully simple: In Week 1, you save $1. In Week 2, you save $2. You continue this pattern until Week 52, where you save $52. By the end of the year, these incremental micro-savings compound into a grand total of $1,378.

- Pro Tip: Treat this weekly transfer like a non-negotiable business expense.

Step 2: Open a Friction-Heavy Savings Account

Do not keep this money in your primary checking account. Open an online HYSA at a different bank (like Ally or Marcus).

- Insider Trick: Do not download the mobile app for this new bank. Adding “friction” (making it harder to access the money quickly) prevents you from dipping into your online earnings fund for impulse purchases.

Step 3: Automate or Schedule Your Transfers

If your bank allows it, set up recurring weekly transfers that automatically increase. If not, set a recurring calendar alarm for every Friday morning titled: “Fund My Financial Freedom.”

Step 4: Audit Your Variable Expenses for Later Weeks

Weeks 1 through 10 are easy. But by Week 40, you are saving $40+ per week. Prepare for this by auditing your subscriptions now. Cancel unused streaming services or negotiate your internet bill so the cash flow is already freed up when the challenge gets tougher.

Step 5: Protect the Capital

When you hit milestones ($100, $500, $1,000), the temptation to spend it on a “reward” will be high. Remember your “why.” This money is strictly for funding your future monetization strategies, not a new pair of shoes.

Income Potential & Earnings Breakdown

How does saving translate to income potential? In personal finance, a penny saved is actually more than a penny earned because it is post-tax money.

If your goal is to generate online earnings, here is how the $1,378 from the 52 Week Money Saving Challenge acts as your launchpad:

| Challenge Phase | Total Saved | What it can fund for your Side Hustle |

|---|---|---|

| Weeks 1 – 12 | $78 | A domain name and 1 year of premium web hosting. |

| Weeks 13 – 26 | $273 | Email marketing software and a premium WordPress theme. |

| Weeks 27 – 40 | $469 | An LLC formation or an entry-level digital marketing course. |

| Weeks 41 – 52 | $558 | Initial Facebook/Google Ads budget to drive traffic. |

| Total (52 Weeks) | **$1,378** | A fully funded, risk-free digital business launch. |

Note: The beauty of this framework is that you are building your business capital without taking on debt or touching your standard paycheck.

Alternative Methods & Variations

Financial strategies aren’t one-size-fits-all. If the standard progressive model doesn’t fit your cash flow, try these niche-specific variations:

- The Reverse 52 Week Challenge: Save $52 in Week 1, $51 in Week 2, working your way down to $1 in Week 52. This is incredible for people who want to capitalize on high motivation at the beginning of the year and have an easier time during the expensive holiday season.

- The Bi-Weekly Approach: If you get paid every two weeks, bundle the weeks together. (e.g., Payday 1: Save $1 + $2 = $3. Payday 26: Save $51 + $52 = $103).

- The “Side Hustle Match” Variation: Instead of cutting expenses to find the weekly deposit, challenge yourself to earn the weekly deposit through gig work, online surveys, or selling old items. This dual-approach builds both savings and active income generation skills simultaneously.

Best Practices & Optimization Tips

To guarantee you make it to Week 52 without quitting, integrate these optimization tips:

- Print a Visual Tracker: Keep a physical checklist on your refrigerator. The dopamine hit of physically crossing off a week is scientifically proven to maintain long-term motivation.

- Leverage Cashback for Late Weeks: Use cashback browser extensions (like Rakuten) for your necessary shopping. Route all cashback directly into your challenge fund to subsidize the heavier $40-$52 weeks at the end of the year.

- Join a Community: Join personal finance or side hustle Facebook groups. Accountability is the ultimate efficiency hack for completing year-long goals.

Common Mistakes to Avoid

Even smart savers stumble during a 52-week timeline. Avoid these critical pitfalls that cause failure rates to spike around Week 20:

- Keeping the Funds Accessible: If your challenge money is linked to your daily debit card, an “emergency” (like wanting takeout pizza) will inevitably arise. Keep it separate.

- Playing Catch-Up: If you miss Week 15, do not try to save double in Week 16. The financial strain will cause you to quit entirely. Forgive the mistake, check off the missed week as a loss, and simply move on to the current week’s goal.

- Lacking a Defined Purpose: Saving $1,378 just to have it sitting there is rarely motivating enough. Assign a strict job to the money—like “This is my YouTube Channel Equipment Fund.”

Long-Term Sustainability & Growth

What happens when you successfully complete the challenge? That is where the real wealth-building begins.

- Reinvestment Strategies: Do not let the $1,378 rot in a low-interest account. Deploy it. Use it to buy income-producing assets, invest in an index fund, or fund the inventory for an e-commerce store.

- The Year 2 Multiplier: In your second year, take the $52/week habit you’ve already built and maintain it permanently. Automatically routing $200+ a month into investments is the bedrock of long-term passive income.

- Diversification: Once you have mastered expense optimization, pivot your energy. Shift your focus entirely toward scaling your revenue streams, knowing your baseline expenses are perfectly managed.

Conclusion

The 52 Week Money Saving Challenge is far more than a simple budgeting trick; it is a systematic framework for building the seed capital necessary to change your life. By starting with just $1, you are taking the first definitive step toward optimizing your profit margins, funding your side hustle, and securing true financial freedom.

Ready to start your journey? Drop a comment below letting us know what side hustle you plan to fund with your $1,378! Subscribe for weekly digital income strategies, share your weekly progress in our community, and download our free 52-Week printable tracker today.

FAQs

How much money can I realistically save with this challenge?

If followed exactly, the standard 52 Week Money Saving Challenge yields exactly $1,378 in 52 weeks. If you place it in a High-Yield Savings Account, it will be slightly more due to compounding interest.

Do I need prior experience with budgeting to start?

Absolutely not. This is arguably the most beginner-friendly financial challenge in existence because Week 1 only requires you to save $1.

What’s the initial investment?

The initial investment is exactly $1. You simply need one dollar, a tracking sheet, and a safe place to store the cash.

What do I do if I can’t afford the higher weeks at the end of the year?

If weeks 45-52 ($45+ per week) are too tight, you can pivot to a randomized approach. Cross off the highest numbers during months you get a bonus or have extra cash, and save the $1-$10 weeks for tighter months.

Is this method still working in the current economy?

Yes. In fact, during periods of inflation, focusing on micro-savings and building an emergency or opportunity fund is one of the most reliable ways to protect your financial future.

What are the risks involved?

There is zero financial risk as you are simply retaining your own money. The only risk is losing motivation, which is why keeping a visual tracker and separating the money from your checking account is crucial.