How to Fund Your New Small Business in 2026: Complete Funding Guide

Did you know that 82% of small businesses fail due to cash flow problems, yet most entrepreneurs spend less than 10 hours researching funding options before launch? If you’re planning to start a small business in 2026, securing adequate funding isn’t just important—it’s the difference between joining the 50% of businesses that survive past five years and becoming another statistic.

The landscape of small business financing has transformed dramatically. Traditional bank loans are no longer your only option. From crowdfunding platforms to alternative lenders, revenue-based financing to government grants, today’s entrepreneurs have access to more diverse funding sources than ever before. Whether you’re launching an online store, opening a local cafe, or developing a tech startup, understanding your financing options is crucial for long-term success.

In this comprehensive guide, we’ll walk you through every viable funding method available in 2026, helping you choose the right combination of financial resources to launch and scale your small business venture. Let’s explore how to turn your entrepreneurial dreams into a well-funded reality.

What You’ll Need to Get Started

Before approaching any funding source, prepare these essential elements:

Business Planning Documents:

- Comprehensive business plan (15-30 pages)

- Executive summary highlighting your value proposition

- Market analysis and competitive research

- Financial projections for 3-5 years

- Break-even analysis

Financial Documentation:

- Personal credit score (aim for 680+ for best options)

- Personal financial statements

- Tax returns (last 2-3 years)

- Business bank account statements if already operating

- Collateral documentation if applicable

Legal Requirements:

- Business registration and licenses

- EIN (Employer Identification Number)

- Business structure documentation (LLC, Corporation, etc.)

- Any relevant permits or certifications

Initial Investment Range:

- Startup costs typically range from $3,000 to $50,000+ depending on industry

- Service-based businesses: $2,000-$10,000

- Retail businesses: $25,000-$100,000+

- Manufacturing: $50,000-$500,000+

Skills Needed:

- Basic financial literacy

- Understanding of business metrics and KPIs

- Pitching and presentation skills

- Networking abilities

- Digital literacy for online applications

Most funding preparation can be done with free resources like SCORE mentorship, SBA online courses, and templates available through business development centers.

Time Investment

Securing small business funding requires patience and strategic planning:

Preparation Phase:

- Business plan development: 40-80 hours

- Financial documentation gathering: 10-20 hours

- Credit score improvement (if needed): 3-6 months

- Market research and validation: 20-40 hours

Application Process:

- Traditional bank loans: 4-12 weeks

- SBA loans: 60-90 days

- Online lenders: 24 hours to 2 weeks

- Crowdfunding campaigns: 30-60 days

- Investor pitching: 3-9 months

- Grant applications: 2-6 months

Realistic Timeline: Most entrepreneurs should plan for 3-6 months from initial preparation to receiving funds. Fast-track options like online lenders or business credit cards can provide capital within days, but often at higher costs. Traditional funding sources require more time but typically offer better terms.

Compared to saving money from a traditional job (which could take years to accumulate startup capital), strategic funding approaches accelerate your launch timeline while preserving personal savings.

Love earning on your own terms? Unlock your potential with these high-income skills and get inspired to share your own success story!

How to Make Money Graphic Design: Your Path to Creative Financial Freedom in 2025

SEO for Beginners: Learn How to Get Free Traffic to Any Website

10 High-Income Skills You Can Learn Online for Free (No Degree Needed)

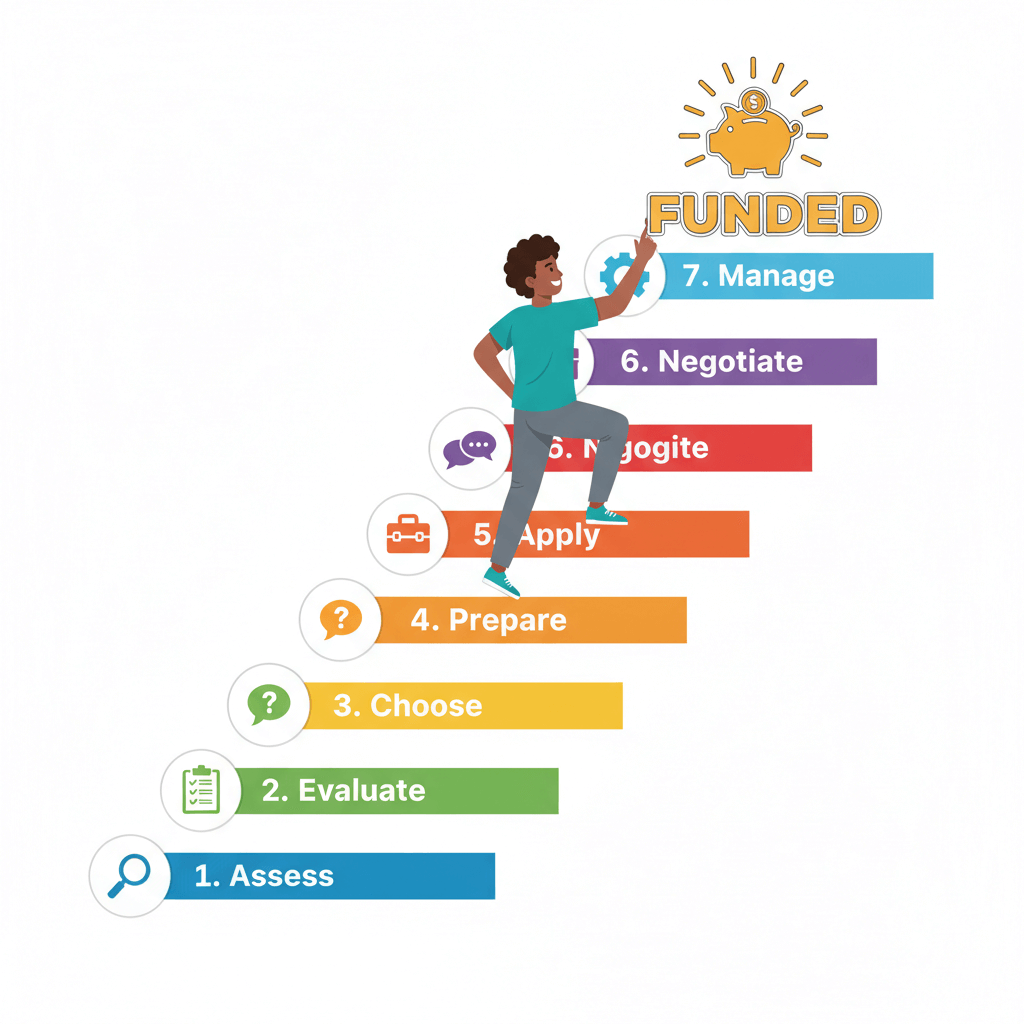

Step-by-Step Implementation Guide

Step 1: Assess Your Funding Needs

Calculate exactly how much capital you need by creating detailed financial projections. Include startup costs, operating expenses for 6-12 months, inventory, equipment, marketing budget, and a 20% buffer for unexpected expenses.

Pro Tip: Separate your funding needs into categories: essential (must-have for launch), growth (needed within first year), and expansion (needed for scaling). This helps you prioritize funding sources and approach.

Step 2: Evaluate Your Funding Eligibility

Review your personal credit score, existing debt obligations, collateral availability, and business viability. Different funding sources have different requirements—knowing where you stand helps you target appropriate options.

Common Question Addressed: If your credit score is below 650, focus first on credit-builder loans, secured credit cards, or alternative lenders that consider factors beyond credit scores.

Step 3: Choose Your Primary Funding Strategy

Select 2-3 funding sources that align with your needs, timeline, and eligibility. Most successful small businesses use a combination approach rather than relying on a single source.

Pro Tip: The best strategy often combines personal investment (showing commitment), one primary external source (bank loan or investor), and one flexible backup option (business line of credit).

Step 4: Prepare Your Funding Application Materials

Create a compelling business plan, polish your executive summary, prepare financial projections with realistic assumptions, gather all required documentation, and practice your pitch if seeking investors.

Insider Trick: Have your business plan reviewed by a SCORE mentor or experienced entrepreneur before submitting applications. Fresh eyes catch gaps that could derail your application.

Step 5: Apply to Multiple Funding Sources

Don’t put all eggs in one basket. Submit applications to 3-5 compatible lenders or funding programs simultaneously. This increases approval odds and gives you negotiating leverage with better terms.

Pro Tip: For bank loans, apply to at least one traditional bank, one credit union, and one online lender to compare rates and terms.

Step 6: Negotiate Terms and Close Funding

Review all offers carefully, comparing interest rates, repayment terms, fees, equity requirements, and flexibility clauses. Don’t accept the first offer—negotiate for better terms using competing offers as leverage.

Common Pitfall: Many entrepreneurs focus solely on approval and overlook unfavorable terms that could cripple their business later. Read the fine print.

Step 7: Establish Financial Management Systems

Once funded, set up proper bookkeeping systems, separate business and personal finances completely, create a cash flow management plan, and establish regular financial review processes.

Pro Tip: Use accounting software like QuickBooks or FreshBooks from day one. Clean financial records make future funding rounds significantly easier.

Income Potential & Earnings Breakdown

While funding itself doesn’t generate income, proper capitalization directly impacts your small business revenue potential:

Adequately Funded vs. Underfunded Businesses:

| Business Type | Well-Funded First Year Revenue | Underfunded First Year Revenue |

|---|---|---|

| E-commerce Store | $150,000-$500,000 | $30,000-$100,000 |

| Service Business | $75,000-$200,000 | $25,000-$75,000 |

| Restaurant | $400,000-$1,000,000 | $150,000-$400,000 |

| Tech Startup | $100,000-$500,000 | $0-$50,000 |

Funding Impact on Growth:

- Businesses with adequate initial funding grow 3.5x faster in year one

- Properly capitalized businesses have 73% higher survival rates

- Well-funded marketing budgets generate 5-10x ROI in customer acquisition

Case Study: A 2024 analysis of 1,000 startups showed that businesses launching with $50,000+ in funding reached profitability 8 months faster on average than those starting with under $10,000, despite being in the same industries.

Return on Investment: The cost of capital varies, but strategic funding typically generates positive ROI within 18-36 months as your small business scales beyond what would be possible with bootstrapping alone.

Alternative Methods & Variations

Bootstrap Funding (Self-Funding): Using personal savings, credit cards, or home equity. Best for: service-based businesses with low startup costs. Pros: retain full ownership, no debt obligations. Cons: personal financial risk, slower growth.

Friends & Family Funding: Borrowing from personal network. Best for: first-time entrepreneurs needing $5,000-$50,000. Pros: flexible terms, faster approval. Cons: relationship risks, often lacks formal structure.

Crowdfunding Campaigns: Platforms like Kickstarter, Indiegogo, or equity crowdfunding sites. Best for: product-based businesses with compelling stories. Average raise: $7,000-$20,000. Success rate: 38% reach funding goals.

Angel Investors & Venture Capital: Professional investors providing capital for equity. Best for: high-growth potential tech and innovative businesses. Typical investment: $25,000-$2,000,000+. Requires giving up 10-30% ownership.

Revenue-Based Financing: Repayment based on percentage of monthly revenue. Best for: businesses with consistent revenue but limited collateral. Pros: flexible payments, faster approval. Costs: typically 1.3-2.5x repayment multiple.

Combining Multiple Sources: Many successful entrepreneurs use a “funding stack”—personal investment (20%), SBA loan (50%), business line of credit (20%), and equipment financing (10%)—to minimize risk while maximizing available capital.

Best Practices & Optimization Tips

Maximize Funding Approval Rates:

- Improve personal credit score above 700 before applying

- Show skin in the game with 10-20% personal investment

- Develop relationships with lenders 6 months before needing capital

- Join industry associations that offer member financing programs

Efficiency Hacks:

- Use SBA’s Lender Match tool to find pre-qualified lenders quickly

- Apply for business credit cards immediately after forming your LLC to start building business credit

- Leverage CDFIs (Community Development Financial Institutions) for faster approval with lower credit requirements

Cost-Saving Strategies:

- Compare at least 5 lenders for interest rate differences (even 1% saves thousands)

- Consider SBA microloans for amounts under $50,000—lower rates than alternatives

- Negotiate origination fees (often reducible by 0.5-1%)

- Choose longer terms for lower monthly payments if cash flow is tight

Advanced Techniques:

- Build business credit separate from personal credit within first 90 days

- Use equipment financing for assets rather than using working capital

- Establish vendor credit lines to preserve cash for operations

- Create a funding pipeline—always have your next funding source identified before needing it

Community Insights: Successful entrepreneurs recommend the “Rule of Thirds”—secure funding equal to one-third personal investment, one-third low-interest debt, and one-third flexible capital (line of credit or investors).

Common Mistakes to Avoid

Underestimating Capital Needs (43% of Failures): Entrepreneurs routinely underestimate funding requirements by 30-50%. Real example: A coffee shop owner budgeted $75,000 but actually needed $120,000, forcing early closure due to inability to sustain operations during the ramp-up period. Prevention: Add 30% buffer to all projections.

Accepting Terrible Terms Out of Desperation: High-interest merchant cash advances (40-200% APR) or predatory loans destroy businesses. Statistics show that businesses paying above 20% interest rates have 3x higher failure rates. Prevention: Never accept funding with APR above 25% except in true emergencies.

Mixing Personal and Business Finances: Using personal accounts for business transactions makes funding applications difficult and creates tax nightmares. This mistake costs small businesses an average of $3,500 annually in missed deductions. Prevention: Open dedicated business banking accounts before receiving any funding.

Ignoring the Cost of Capital: Many entrepreneurs focus only on approval, not total cost. A $50,000 loan at 12% costs $16,500 in interest over 5 years versus $9,000 at 7%. Prevention: Calculate total repayment amount, not just monthly payment.

Waiting Until Desperate to Seek Funding: Applying for financing when cash-strapped results in worse terms and lower approval rates. Lenders prefer funding healthy businesses, not rescuing struggling ones. Prevention: Seek capital 6 months before you’ll need it.

Neglecting Business Credit Building: Relying solely on personal credit limits future funding options. Lessons from successful practitioners: Start building business credit immediately by opening vendor accounts, getting a business credit card, and ensuring vendors report payments to business credit bureaus.

Long-Term Sustainability & Growth

Maintaining Strong Funding Relationships: Pay all obligations on time (even early) to build credibility for future funding needs. Communicate proactively with lenders about business progress. Most successful small businesses return to their initial funding source for growth capital, receiving better terms due to proven track record.

Reinvestment Strategies: Once profitable, allocate 15-25% of profits back into business growth. This reduces dependence on external funding and increases business valuation. Consider the “70-20-10 rule”—70% to operations, 20% to growth investments, 10% to emergency reserves.

Diversification Recommendations: Don’t rely on a single funding source long-term. Successful small businesses develop multiple capital access points: established banking relationship, business line of credit, vendor credit terms, and retained earnings. This creates financial resilience during economic downturns.

Automation Opportunities: Set up automatic payments to build payment history. Use financial management software that integrates with your accounting system. Implement early warning dashboards that alert you to cash flow issues 60 days in advance, giving time to secure additional funding if needed.

Future-Proofing Your Funding Strategy: Build business credit separate from personal credit to access larger capital amounts. Document all business processes and financials professionally to increase business valuation for future investor funding. Maintain a “funding roadmap” showing planned capital needs for next 3 years, allowing you to approach funding sources strategically rather than reactively.

Scaling Your Funding Approach: As your small business grows, funding sources should evolve: startup phase (personal savings, friends/family, microloans) → growth phase (SBA loans, business lines of credit) → expansion phase (commercial loans, investors, revenue-based financing). Businesses that scale funding appropriately grow 2.5x faster than those stuck in startup funding mode.

Conclusion

Funding your small business in 2026 requires strategic planning, thorough preparation, and understanding of diverse capital sources available to modern entrepreneurs. From traditional SBA loans to innovative revenue-based financing, the key is matching funding sources to your specific business needs, timeline, and growth objectives. Remember that adequate capitalization isn’t just about launching—it’s about sustaining operations through the critical early months and positioning your business for long-term success. With 73% higher survival rates for well-funded businesses, investing time in securing proper funding is one of the most important decisions you’ll make as an entrepreneur.

Ready to start your funding journey? Download our free Small Business Funding Checklist and join our community of funded entrepreneurs sharing their success strategies. Drop your questions in the comments below—we respond to every one!

FAQs

Should I give up equity or take on debt?

This depends on your growth trajectory and comfort with partners. Debt makes sense when: you can afford monthly payments, want to retain full ownership, and have predictable revenue to service loans. Equity funding (investors) works better when: you need large capital amounts, want strategic guidance from experienced investors, anticipate rapid growth that justifies dilution, or lack cash flow for debt payments. Many successful businesses use a combination approach.

Can I get funding with bad personal credit?

Yes, though options are more limited and expensive. Consider: alternative lenders focusing on business performance over credit scores (typically require 550+ credit), equipment financing using the purchased asset as collateral, invoice factoring based on customer creditworthiness, or revenue-based financing tied to business sales rather than personal credit. Simultaneously work on improving your credit score for better future funding options.

What are the main risks of taking on business debt?

Primary risks include: personal liability if you’ve personally guaranteed loans, cash flow strain from monthly payments during slow periods, potential asset loss if using collateral, and limiting future borrowing capacity. However, strategic debt used to grow revenue faster than interest costs can significantly accelerate business success. The risk lies in over-leveraging or using expensive debt (above 15% APR) that becomes unsustainable.

Are these small business funding methods still working in 2026?

Yes, but the landscape continues evolving. Traditional bank loans remain available but more competitive. Alternative lending has expanded significantly, offering faster approval with moderate rates. Government-backed SBA loans continue supporting small businesses with favorable terms. The key is matching your business profile to the right funding source and maintaining strong financial fundamentals regardless of method chosen.

How long until I receive funding after applying?

Timeline varies by source: online lenders (24 hours-2 weeks), traditional bank loans (4-12 weeks), SBA loans (60-90 days), and investor funding (3-9 months). Fast funding typically comes with higher costs. Plan your application timeline backward from when you need capital, adding buffer time for potential delays or additional documentation requests.

What’s the typical initial investment required from business owners?

Most lenders expect entrepreneurs to contribute 10-30% of total startup costs from personal funds. This “skin in the game” demonstrates commitment and reduces lender risk. For a $50,000 funding need, plan to personally invest $5,000-$15,000. Some programs like SBA microloans may have lower personal investment requirements.

Do I need prior business experience to get funding?

Not necessarily, but it helps significantly. First-time entrepreneurs can still secure funding through SBA microloans, crowdfunding, or alternative lenders that focus on business viability rather than personal track record. Partnering with an experienced advisor or mentor strengthens applications. Many lenders value industry experience even if you haven’t owned a business before.

How much money do I realistically need to start a small business?

Startup costs vary dramatically by industry. Service-based businesses can launch with $2,000-$10,000, while retail businesses typically need $25,000-$100,000+. Create detailed financial projections including 6-12 months of operating expenses beyond initial setup costs. Most experts recommend having 1.5x your calculated amount to account for unexpected expenses.

Your Feedback Informs Our Service

This article is a lifesaver! The 7-step guide is exactly what I needed. Breaking down the funding into “essential,” “growth,” and “expansion” categories was a game-changer for my budgeting. The pro tip about using a combination of funding sources instead of relying on one gave me a much more realistic strategy. Finally, a guide that focuses on action, not just theory.

As someone with a great idea but no finance background, this was incredibly clear and reassuring. The step about evaluating eligibility saved me from wasting time on applications I’d never get. I especially appreciated the “Common Question Addressed” about low credit scores—it made me feel like the article was written for real people with real problems. The tip to use accounting software from day one is going straight onto my to-do list!

I wish I had this guide when I started my first business years ago. It perfectly balances modern strategies (like alternative lenders) with timeless, sound advice (like negotiating terms). The “Insider Trick” to have a SCORE mentor review your plan is pure gold and something many new founders overlook. This is a comprehensive, no-nonsense roadmap that cuts through the noise. Highly recommended for any serious entrepreneur.