Money Saving Strategies: Smart Tips to Build Your Savings

Did you know that an alarming 63% of adults live paycheck to paycheck simply because they lack structured, intentional money saving strategies? It is a staggering statistic that keeps highly capable individuals trapped in a cycle of financial stress, unable to pursue their dreams or invest in their future.

However, mastering your personal finances is the most historically proven pathway to achieving true financial freedom. Whether your goal is to build an emergency fund, create seed capital for a lucrative side hustle, or transition to a work from home lifestyle permanently, retaining the money you make is just as important as earning it.

In this comprehensive guide, we are cutting through the generic advice like “stop buying coffee.” We will deliver a realistic, data-driven roadmap to help you build, launch, and scale a bulletproof personal budget. Let’s explore exactly what it takes to plug the leaks in your wallet, maximize your income potential, and transform your saved cash into sustainable revenue streams.

What You’ll Need to Get Started

Contrary to popular belief, implementing effective money saving strategies doesn’t require a degree in finance or an expensive financial advisor. You simply need a foundational toolkit to track your cash flow and ensure your monetization strategies are working for you, not against you.

- Budgeting and Tracking Tools: * Premium: YNAB (You Need A Budget) – $14.99/month (Highly effective for zero-based budgeting).

- Free Alternatives: Rocket Money, EveryDollar, or a customized Google Sheets template.

- Banking Setup: * A High-Yield Savings Account (HYSA) like Ally, SoFi, or Marcus to ensure your savings earn competitive interest.

- Essential Skills: * Basic spreadsheet literacy, emotional discipline regarding impulse purchases, and the willingness to negotiate existing bills.

- Initial Investment: * $0. In fact, your initial “investment” is simply the time it takes to review your bank statements.

Love watching your savings grow? Check out these top saving strategies and get inspired to share your own smart money habits!

How to Save Money on Electricity: 15 Surprisingly Simple Tips That Could Cut Your Bills in Half

Best Cashback Apps: How I Earn Over $500 Back a Year on Normal Shopping

How to Lower Your Bills: The Ultimate Guide to Negotiating Your Cable, Phone, and Insurance Rates

Master Your No Spend Challenge: The Ultimate Guide to Rules, Tips, and Incredible Savings in 2025

50 Easy Ways to Save Money on Groceries Without Coupons: Transform Your Food Budget Today

Time Investment

Building a sustainable cushion of savings is a marathon, not a sprint. Setting realistic time expectations is crucial to avoid early frustration and ensure you stay the course toward financial freedom.

- Setup Time Required: Expect to spend 2 to 3 hours initially to gather your bank statements, categorize your past 30 days of spending, and set up your tracking app or spreadsheet.

- Daily/Weekly Commitment: Dedicate 10–15 minutes per week to reconcile your accounts, review your budget, and track your progress.

- Timeline to First “Earnings”: Most beginners see their first tangible results (a surplus of cash at the end of the month) within 30 to 60 days of consistent effort.

Compare this to trying to increase your online earnings through a new business, which can take months to become profitable. Implementing strict money saving strategies provides an immediate, guaranteed return on your time investment.

Step-by-Step Implementation Guide

Follow these actionable steps to get your financial house in order and start accumulating wealth.

Step 1: Conduct a Brutal Financial Audit

Before you can save, you must know where your money is going. Print out your last three months of bank and credit card statements. Highlight every non-essential expense. You cannot improve what you do not measure.

- Pro Tip: Categorize expenses into “Needs,” “Wants,” and “Debt/Savings.” This visual breakdown is often the wake-up call beginners need.

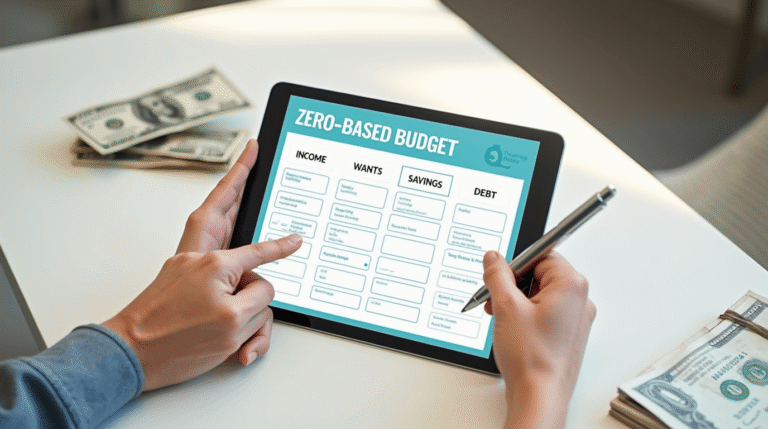

Step 2: Implement the Zero-Based Budget

Give every single dollar a job before the month begins. If you earn $4,000 a month, your expenses, savings, and investments should add up to exactly $4,000.

- Pro Tip: Treat your savings contribution like a mandatory utility bill. Pay yourself first.

Step 3: Automate Your Savings

Human willpower is flawed. Set up an automatic transfer from your checking account to your High-Yield Savings Account on the day you get paid. Out of sight, out of mind.

Step 4: Slash the “Big Three” Expenses

Housing, transportation, and food make up 70% of the average budget. Negotiate your rent (or consider house hacking), shop around for cheaper car insurance, and substitute expensive takeout with strategic meal planning.

Step 5: Redirect Savings into Digital Income

Once you have a 3-6 month emergency fund, take your monthly savings and use it as seed capital. Invest it in index funds, or use it to fund a low-cost side hustle that generates passive income online.

Income Potential & Earnings Breakdown

In personal finance, a penny saved is genuinely a penny earned—in fact, it’s better, because saved money is tax-free. Here is a realistic look at how optimizing your personal “profit margins” translates into tangible wealth:

| Saving Action | Estimated Monthly Savings | Annual “Income Potential” | 10-Year Value (Invested at 7%) |

|---|---|---|---|

| Canceling Unused Subs | $40 – $100 | $480 – $1,200 | $17,000+ |

| Meal Planning/Less Dining Out | $150 – $400 | $1,800 – $4,800 | $68,000+ |

| Negotiating Insurance/Bills | $30 – $80 | $360 – $960 | $13,000+ |

| Automated 10% Salary Deduction | $300 – $600 | $3,600 – $7,200 | $102,000+ |

Payment Structures: Unlike traditional revenue streams where you wait for clients to pay you, the “payments” from money saving strategies are immediate. By spending less, you instantly increase the cash flow residing in your checking account.

Alternative Methods & Variations

If traditional line-item budgeting doesn’t suit your personality, consider these lucrative variations to achieve the same goal:

- The 50/30/20 Rule: A simpler approach where 50% of your income goes to Needs, 30% to Wants, and 20% strictly to Savings and Debt Payoff.

- Cash Stuffing (The Envelope System): Withdraw your weekly allowance in cash and divide it into labeled envelopes (Groceries, Gas, Fun). When the envelope is empty, you stop spending.

- No-Spend Challenges: Gamify your savings by committing to a “No-Spend November” or a 30-day challenge where you only buy absolute necessities. It’s a great way to quickly hoard cash to launch a work from home business.

Best Practices & Optimization Tips

To maximize your savings rate and outpace inflation, implement these optimization strategies:

- Leverage Cashback Apps: Use free tools like Rakuten, Ibotta, or Honey for purchases you were already planning to make. It’s essentially free digital income.

- Implement the 48-Hour Rule: Before making any non-essential purchase over $50, force yourself to wait 48 hours. This efficiency hack kills 90% of impulse buying.

- Optimize Your Banking: Never leave large amounts of cash in a traditional checking account earning 0.01%. Move it to a HYSA to leverage the power of compound interest.

- Community Accountability: Join Reddit communities like r/personalfinance or r/Fire (Financial Independence, Retire Early) to stay motivated and learn advanced techniques from experienced savers.

Common Mistakes to Avoid

The path to building successful financial freedom is often paved with the failures of others. Avoid these fatal errors in your money saving journey:

- Succumbing to Lifestyle Creep: Earning a raise and immediately upgrading your car or apartment is the #1 reason high earners stay broke. When your income goes up, your savings rate should go up, not your lifestyle.

- Failing to Build an Emergency Fund First: Investing in stocks or a side hustle before having 3 months of living expenses saved is a recipe for disaster. One medical bill can wipe you out.

- Depriving Yourself Completely: Budgeting is like dieting. If you cut out 100% of your “fun” spending, you will eventually binge spend. Allocate a small, guilt-free allowance to keep yourself sane.

- Ignoring High-Interest Debt: Saving money in an account earning 4% while carrying credit card debt that costs you 24% is mathematical self-sabotage. Always clear toxic debt first.

Long-Term Sustainability & Growth

Once you secure a comfortable emergency fund and master your daily spending, the goal shifts from “saving” to “investing and growing.”

To future-proof your finances, you must pivot. You cannot simply save your way to massive wealth due to inflation. Reinvestment strategies are key. Take the $500 a month you successfully learned to save, and deploy it into income-producing assets.

Whether that means dollar-cost averaging into S&P 500 index funds, purchasing real estate, or funding an online earnings venture, diversification is crucial. Using your meticulously saved cash to build automated, passive revenue streams is how simple budgeting transforms into true, generational wealth.

Conclusion

Implementing robust money saving strategies is not about punishing yourself; it is the ultimate act of paying your future self. By tracking your expenses, avoiding lifestyle creep, and automating your wealth-building habits, you create the financial runway necessary to take risks, start businesses, and achieve unparalleled freedom.

Ready to start your journey? Drop your biggest budgeting challenge or question in the comments below! Don’t forget to bookmark this page, share your progress in our community, and subscribe to our newsletter for weekly financial tips and monetization strategies.

FAQs

How much money can I realistically save each month?

While it depends on your income, the average beginner who strictly audits their budget can usually find between $200 to $500 a month in wasteful spending to redirect into savings.

Do I need prior financial experience to start budgeting?

No prior experience is necessary. Modern apps like YNAB or Rocket Money do the heavy lifting for you. You simply need the discipline to stick to the limits you set for yourself.

What’s the initial investment to start saving?

Zero dollars! The only requirement is an investment of your time to review your past spending and set up a basic tracking system.

How long until I see results?

If you actively track your expenses and eliminate impulse purchases, you will see a noticeable surplus in your bank account by your very next pay cycle (typically within 30 days).

Is this method still working in 2026?

Absolutely. Regardless of the economic climate or inflation rates, the fundamental mathematics of spending less than you earn remains the undisputed cornerstone of personal wealth building.

What are the risks involved?

There is zero financial risk in saving money. The only risk is the “opportunity cost” of leaving too much cash in a low-yield account where inflation outpaces your interest rate. Once your emergency fund is built, transition those savings into investments.

Disclaimer: The financial figures discussed in this guide are estimates based on average consumer habits. Personal finance is highly individual. Success requires consistent effort and discipline. This content is for educational purposes and is not formal financial advice.

Your Feedback Informs Our Service

There are no reviews yet. Be the first one to write one.