Zero-Based Budgeting: A Step-by-Step Guide for Beginners

Picture yourself sitting at your kitchen table at 2 AM, surrounded by crumpled receipts and bank statements. Your heart pounds as you realize—once again—that your carefully planned budget has completely fallen apart. You started the month with such good intentions, tracking expenses for the first week, maybe two. But somewhere between that unexpected car repair and your friend’s birthday dinner, everything went sideways.

Does this scene feel painfully familiar? You’re certainly not walking this path alone. Recent financial surveys reveal that nearly 64% of Americans struggle to stick with their budgeting plans beyond the first month. The harsh reality? Most traditional budgeting methods set you up for disappointment from day one.

But what if someone told you there’s a revolutionary approach that successful Fortune 500 companies use to eliminate waste and maximize profits? A method so precise that it forces every single dollar to justify its existence? This isn’t just another budgeting trend—it’s zero-based budgeting, and it’s about to completely reshape how you think about money management.

What Is Zero-Based Budgeting and Why It’s Different from Traditional Budgeting Methods

Zero-Based Budgeting Tool

Your goal: Give every dollar a job until the balance is $0.

🎉 Perfect Zero!

You’ve successfully given every dollar a job. This is the foundation of financial success.

Get Your ZBB Spreadsheet

Ready to track this for real? Download our Zero-Based Budget Template for Excel or Google Sheets.

Understanding Zero-Based Budgeting Fundamentals

Zero-based budgeting operates on a beautifully simple premise: every month, you start with a clean slate. Unlike conventional budgeting that builds upon previous months' spending patterns, zero-based budgeting demands that you justify every single expense from scratch. Your mission? Make your income minus your expenses equal exactly zero.

This doesn't mean you spend every penny frivolously. Instead, you're strategically assigning each dollar a specific job—whether that's covering rent, building an emergency fund, or enjoying a night out with friends. The key difference lies in intentionality. Traditional budgets often leave room for "leftover" money that mysteriously disappears, while zero-based budgeting ensures every dollar has a predetermined purpose.

The Psychology Behind Why Zero-Based Budgeting Works

Your brain craves structure and clear boundaries, especially when dealing with abstract concepts like money. Zero-based budgeting taps into powerful psychological principles that traditional budgeting methods often ignore.

When you're forced to assign every dollar before spending it, you engage your prefrontal cortex—the part of your brain responsible for planning and decision-making. This mental exercise creates what behavioral economists call "cognitive friction," making you pause and consider each financial choice deliberately.

Research from Duke University demonstrates that people who use intentional budgeting methods (like zero-based budgeting) reduce impulsive spending by up to 23% compared to those using traditional tracking methods. The reason? You're making spending decisions when you're calm and rational, not in the heat of the moment when emotions run high.

Love financial peace of mind? Check out these top budgeting methods and get inspired to share your own financial game plan!

How to Create a Bi-Weekly Budget That Actually Works (Perfect If You Get Paid Every Two Weeks)

7 Best Budgeting Apps of 2024 to Take Control of Your Money

The 50/30/20 Rule: Master Your Money with This Simple Budgeting Method for Beginners

How to Create a Zero-Based Budget That Actually Works

Zero-Based Budgeting: Transform Your Finances with a Budget That Actually Works in 2025

Step-by-Step Guide: How to Create Your First Zero-Based Budget

Step 1 - Calculate Your True Monthly Income

Before allocating a single dollar, you need crystal-clear clarity on exactly how much money flows into your accounts each month. This step requires more precision than you might initially think.

Start with your primary income source, but don't just look at your gross salary. Focus on your take-home pay—the actual amount that hits your checking account after taxes, insurance premiums, and retirement contributions. If you're paid bi-weekly, multiply one paycheck by 26, then divide by 12 to get your true monthly average.

Don't overlook additional income streams:

- Side hustle earnings (freelancing, rideshare, delivery services)

- Investment dividends or rental income

- Child support or alimony payments

- Regular gifts from family members

- Cashback rewards from credit cards

- Small business profits

For irregular income, use the lowest amount you typically earn in a month as your baseline. When extra money arrives, you'll have a predetermined plan for where it goes—but your core budget remains stable and achievable.

Step 2 - List Every Single Expense Category

This step separates zero-based budgeting champions from those who give up after month one. You must capture every expense, no matter how small or infrequent.

Create three distinct categories:

Fixed Expenses (same amount each month):

- Mortgage or rent payments

- Insurance premiums (health, auto, life)

- Loan payments (student loans, car payments)

- Cell phone bills

- Internet and streaming services

- Gym memberships

Variable Expenses (amounts change monthly):

- Groceries and household supplies

- Gasoline and transportation

- Entertainment and dining out

- Clothing and personal care

- Utilities (if they fluctuate seasonally)

Irregular Expenses (occur quarterly or annually):

| Expense Type | Typical Frequency | Monthly Allocation Strategy |

|---|---|---|

| Car registration/inspection | Annual | Divide by 12 months |

| Holiday gifts | Annual | Save year-round |

| Home maintenance | Seasonal | 1-2% of home value annually |

| Medical deductibles | As needed | Based on health history |

| Professional development | Annual | Career investment fund |

Step 3 - Assign Every Dollar a Purpose

Now comes the heart of zero-based budgeting: the allocation process. Start with your most critical expenses and work your way down to discretionary spending.

Follow this priority hierarchy:

- Basic survival needs (housing, utilities, minimum food)

- Transportation (car payments, gas, maintenance)

- Minimum debt payments (credit cards, loans)

- Emergency fund (until you reach $1,000 minimum)

- Insurance premiums (health, auto, renters/homeowners)

- Additional debt payments (accelerated payoff)

- Retirement savings (at least employer match)

- Other savings goals (vacation, home down payment)

- Entertainment and discretionary spending

Remember: you're not depriving yourself of fun. You're simply ensuring your fundamental needs are covered before allocating money to wants.

Step 4 - Make Adjustments Until You Reach Zero

Here's where most people hit their first roadblock. Your initial attempt will rarely balance perfectly. Your expenses might exceed your income by $200, $500, or even more. Don't panic—this is completely normal and actually valuable information.

When expenses exceed income, you have two options:

Option 1: Reduce Expenses

- Challenge every variable expense (Do you really need five streaming services?)

- Negotiate fixed expenses (Call insurance companies for better rates)

- Eliminate non-essential categories temporarily

- Find creative alternatives (library instead of bookstore, home workouts instead of gym)

Option 2: Increase Income

- Pick up extra shifts or overtime

- Start a side hustle (driving for apps, freelance services)

- Sell items you no longer need

- Ask for a raise or promotion at work

Most successful zero-based budgeters combine both approaches, trimming unnecessary expenses while exploring income opportunities.

Common Zero-Based Budgeting Mistakes (And How to Avoid Them)

Mistake #1 - Being Too Restrictive in the Beginning

Enthusiasm can be your enemy when starting zero-based budgeting. Many people create impossibly strict budgets that eliminate all enjoyment, setting themselves up for spectacular failure within weeks.

Your budget should feel challenging but sustainable. If you typically spend $400 monthly on restaurants and entertainment, don't slash it to $50 overnight. Instead, reduce it to $300 for the first month, then gradually decrease as you develop better habits.

Behavioral research shows that gradual changes have an 80% higher success rate than dramatic overhauls. Give yourself permission to be human while still making meaningful progress.

Mistake #2 - Forgetting Irregular Expenses

December arrives, and suddenly you're scrambling to find $800 for holiday gifts. Your car registration comes due, and you don't have the $150 ready. Sound familiar? These "surprise" expenses derail more budgets than any other single factor.

Create a comprehensive list of irregular expenses:

- Vehicle maintenance and repairs

- Medical co-pays and prescriptions

- Home maintenance projects

- Professional development courses

- Pet veterinary care

- Holiday and birthday gifts

- Annual subscriptions and memberships

- Tax preparation fees

Divide each annual expense by 12 and save that amount monthly. Your December self will thank you when gift-giving season arrives stress-free.

Mistake #3 - Not Having a Buffer Category

Life rarely follows your budget exactly. Your grocery bill might be $20 higher than expected, or you might need to buy a last-minute birthday card. Without a buffer category, these small overages can create a domino effect of budget failures.

Allocate 2-5% of your income to a "miscellaneous" or "buffer" category. This small cushion handles minor overruns without requiring major budget adjustments. Think of it as insurance for your budget's success.

Zero-Based Budgeting Tools and Resources to Streamline the Process

Best Apps for Zero-Based Budgeting

Technology can transform zero-based budgeting from a tedious chore into a streamlined process. Here's an honest comparison of the top options:

| App Name | Monthly Cost | Zero-Based Features | Learning Curve | Best For |

|---|---|---|---|---|

| YNAB | $14 | Excellent - Built specifically for zero-based | Moderate | Serious budgeters willing to invest |

| EveryDollar | Free/$17 premium | Good - Dave Ramsey methodology | Easy | Beginners and debt payoff focus |

| Mint | Free | Poor - Traditional tracking focused | Easy | General expense tracking only |

| Spreadsheet | Free | Excellent - Complete customization | Varies | DIY enthusiasts and advanced users |

YNAB (You Need A Budget) stands as the gold standard for zero-based budgeting apps. Its "give every dollar a job" philosophy aligns perfectly with zero-based principles. The app forces you to allocate money before spending and automatically adjusts when you overspend in categories.

EveryDollar, created by financial guru Dave Ramsey's team, offers a simpler approach. The free version provides basic zero-based budgeting functionality, while the premium version connects to your bank accounts for automatic transaction importing.

Creating Your Own Zero-Based Budget Spreadsheet

Sometimes the best tool is the one you build yourself. A custom spreadsheet gives you complete control over categories, formulas, and layout while costing absolutely nothing.

Essential columns for your zero-based budget spreadsheet:

- Income sources (with individual amounts and total)

- Expense categories (with budgeted amounts)

- Actual spending (tracked throughout the month)

- Remaining balance (budgeted minus actual)

- Running total (to ensure you hit zero)

Zero-Based Budgeting for Couples

Money conversations rank among the most challenging discussions couples face, but zero-based budgeting can actually strengthen your financial partnership when approached correctly.

Start with a "financial values" discussion before diving into numbers. What matters most to each of you? Security? Experiences? Future goals? Understanding these underlying priorities prevents arguments about specific budget allocations.

Assign roles based on strengths and interests:

- One person might excel at tracking daily expenses

- The other might prefer researching ways to reduce fixed costs

- Both should participate in monthly budget reviews and adjustments

Establish spending limits that don't require consultation. Maybe you agree that individual purchases under $50 don't need discussion, but anything above that threshold requires a conversation. This balance preserves autonomy while maintaining accountability.

Advanced Zero-Based Budgeting Strategies for Long-Term Success

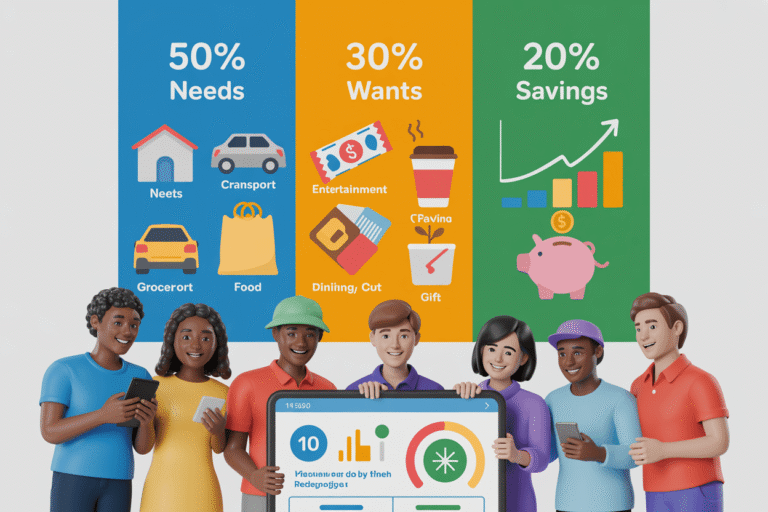

Incorporating the 50/30/20 Rule into Zero-Based Budgeting

The popular 50/30/20 rule (50% needs, 30% wants, 20% savings) can provide helpful guardrails within your zero-based framework. However, don't treat these percentages as rigid requirements—adjust them based on your specific situation.

| Category | Percentage Range | Zero-Based Application |

|---|---|---|

| Needs | 40-60% | Housing, utilities, groceries, transportation, minimum debt payments |

| Wants | 20-40% | Entertainment, dining out, hobbies, non-essential shopping |

| Savings/Debt | 20-40% | Emergency fund, retirement, extra debt payments, goal-specific savings |

If you're paying off high-interest debt, you might allocate 40% to debt payments and only 20% to wants. If you're financially stable with good emergency savings, perhaps 35% goes to wants and 15% to additional savings goals.

The key is intentional allocation that reflects your current priorities and financial situation.

Zero-Based Budgeting for Variable Income

Freelancers, commission-based salespeople, and seasonal workers face unique budgeting challenges, but zero-based budgeting can provide stability amid income fluctuations.

Strategy 1: Conservative Base Budget Use your lowest typical monthly income as your baseline budget. This covers all essential expenses during lean months. When higher-income months occur, allocate the extra money according to predetermined priorities:

- Build emergency fund to 6-8 months of expenses (higher than typical recommendations)

- Pay down debt aggressively

- Save for known slow periods

- Invest in business development or education

- Enjoy lifestyle improvements (only after other priorities are met)

Strategy 2: Income Smoothing Account Create a separate "income smoothing" account that acts as your employer. During high-income months, deposit excess earnings. During low-income months, pay yourself from this account to maintain consistent monthly income.

Scaling Zero-Based Budgeting as Your Income Grows

One of zero-based budgeting's greatest strengths is preventing lifestyle inflation from silently sabotaging your financial progress. When your income increases, you have a framework for strategic allocation rather than unconscious spending increases.

Before adjusting any categories, ask yourself:

- Are your current financial goals fully funded?

- Is your emergency fund adequate for your new income level?

- Are you maximizing tax-advantaged retirement accounts?

- What would bring you the most long-term satisfaction?

Consider the "happiness research" when allocating raises: studies show that experiences typically provide more lasting satisfaction than material purchases, and giving money away can increase personal happiness levels significantly.

Real Success Stories: How Zero-Based Budgeting Changed Lives

Case Study 1: From $50,000 Debt to Financial Freedom

Sarah and Mike, a married couple from Denver, faced a financial crisis that many Americans would find familiar. Combined student loan debt of $85,000, credit card balances totaling $15,000, and a car loan of $18,000 left them feeling hopeless despite earning $95,000 annually.

Their breakthrough came when Sarah discovered zero-based budgeting through a personal finance podcast. Initially skeptical, Mike agreed to try it for three months.

Their zero-based budgeting transformation:

Month 1-3: Tracked every expense and created their first zero-based budget. They discovered $800 monthly in "leakage"—small purchases that added up significantly.

Month 4-12: Allocated the recovered $800 toward debt payments while maintaining a modest entertainment budget. They paid off all credit cards.

Month 13-30: Focused intensively on student loans, adding an additional $400 monthly by reducing their entertainment and clothing budgets temporarily.

Results after 30 months: Complete debt freedom except their mortgage, emergency fund of $25,000, and newfound confidence in their financial decision-making.

"The magic wasn't in the restriction," Sarah explains. "It was in the intentionality. We still went out to dinner and took vacations—we just planned for them instead of hoping we'd have money left over."

Case Study 2: Young Couple Saves for First Home

James and Lisa, both 26, earned a combined $78,000 annually but felt trapped in their expensive urban apartment. Their goal seemed impossible: save $45,000 for a down payment and closing costs within two years while maintaining their quality of life.

Their zero-based budgeting approach:

- Calculated exactly how much they needed to save monthly: $1,875

- Identified their largest expense categories: rent ($2,200), food ($800), and entertainment ($600)

- Made strategic adjustments: moved to a smaller apartment saving $400 monthly, meal prepped to reduce food costs by $300, and chose free/low-cost entertainment options saving $200

- Allocated the $900 monthly savings directly to their house fund

Additional strategies:

- Sold unnecessary possessions for an extra $3,000

- Used tax refunds and bonuses exclusively for the house fund

- Picked up occasional freelance work for accelerated savings

Results: Purchased their first home after 22 months with $47,000 saved—exceeding their original goal despite facing an unexpected $2,500 car repair during the process.

What the Data Says About Zero-Based Budgeting Success

Research from financial institutions and budget app companies reveals compelling statistics about zero-based budgeting effectiveness:

- Users reduce overall spending by an average of 19% within six months

- Emergency fund completion rates are 340% higher compared to traditional budgeting methods

- Debt payoff accelerates by an average of 14 months

- Long-term budgeting adherence (12+ months) reaches 67% versus 23% for conventional budgeting

Perhaps most importantly, 78% of zero-based budgeters report feeling "in control" of their finances after six months, compared to 34% using other budgeting methods.

Troubleshooting Your Zero-Based Budget When Life Happens

Handling Unexpected Expenses

Life specializes in throwing curveballs at your carefully planned budget. Your car breaks down, your pet needs emergency surgery, or your child requires unexpected school supplies. These moments test your zero-based budgeting system's resilience.

Immediate response strategy:

- Don't abandon your budget—adjust it

- Use your emergency fund if the expense qualifies (urgent and necessary)

- Reallocate money from other categories for smaller unexpected costs

- Document what happened and adjust future budgets accordingly

Emergency fund integration: Your emergency fund isn't separate from zero-based budgeting—it's a crucial component. In your monthly budget, treat emergency fund contributions like any other essential expense until you reach your target amount (typically 3-6 months of expenses).

When you use emergency funds, immediately adjust your budget to include replenishment as a priority expense. This ensures your safety net remains intact for future emergencies.

Seasonal Budget Adjustments

Your zero-based budget shouldn't remain static throughout the year. Seasonal variations in expenses and income require proactive adjustments to maintain effectiveness.

Holiday season planning (October-December):

- Increase gift category starting in January (spread costs across 12 months)

- Reduce other discretionary spending during high-expense months

- Plan for higher utility costs in winter months

- Budget for holiday travel expenses

Summer adjustments:

- Account for higher cooling costs

- Plan vacation and summer activity expenses

- Prepare for potential income changes (teachers, seasonal workers)

- Budget for increased fresh produce costs but lower utility bills

Back-to-school period (August-September):

- Allocate funds for school supplies, clothing, and fees

- Prepare for schedule changes affecting childcare costs

- Plan for fall activity registrations and equipment

Create a "seasonal expense calendar" that helps you anticipate and prepare for these predictable variations.

Zero-Based Budgeting During Financial Hardship

Economic downturns, job losses, or medical emergencies can devastate even well-planned budgets. However, zero-based budgeting principles become even more valuable during financial hardship.

Crisis budgeting priorities:

- Shelter: Rent/mortgage, basic utilities

- Food: Focus on nutritional necessities, not preferences

- Transportation: Maintain ability to work/seek employment

- Minimum debt payments: Protect credit score for recovery period

Temporary adjustments:

- Suspend all discretionary spending until stability returns

- Negotiate payment plans with creditors before missing payments

- Explore community resources (food banks, utility assistance programs)

- Consider temporary income sources (gig work, selling possessions)

Maintaining motivation: Financial hardship can feel overwhelming, but remember that zero-based budgeting gives you maximum control over your limited resources. Every dollar you manage wisely extends your financial runway and improves your recovery prospects.

Conclusion

Zero-based budgeting isn't just another financial strategy—it's a complete mindset transformation that puts you in the driver's seat of your financial destiny. Unlike passive budgeting methods that simply track where your money went, zero-based budgeting ensures every dollar serves your goals before you spend it.

The journey won't always be smooth. Your first zero-based budget might take several hours to create and multiple revisions to balance. You'll face moments of frustration when unexpected expenses arise or when you realize you've been unconsciously spending money on things that don't truly matter to you. These challenges aren't signs of failure—they're evidence that the system is working, forcing you to confront financial realities you might have previously ignored.

What makes zero-based budgeting revolutionary is its flexibility within structure. You're not following someone else's predetermined categories or percentages. Instead, you're creating a personalized financial blueprint that reflects your unique values, goals, and circumstances. Want to spend more on travel? Allocate accordingly. Prioritizing debt freedom? Direct every available dollar toward payments. Focused on building wealth? Maximize your investment contributions.

The success stories aren't anomalies—they're predictable outcomes of intentional financial management. When you give every dollar a specific job and hold yourself accountable for those decisions, remarkable changes become inevitable. Debt disappears faster, savings grow more consistently, and financial stress decreases dramatically.

Your financial transformation starts with a single decision: the commitment to try zero-based budgeting for just three months. Don't worry about perfection. Focus on progress, learning, and gradual improvement. Track your results, celebrate small victories, and adjust your approach as you discover what works best for your situation.

The tools exist, the strategies are proven, and thousands of people have already walked this path successfully. The only question remaining is whether you're ready to take complete control of your financial future.

Frequently Asked Questions About Zero-Based Budgeting

What is zero-based budgeting and how does it differ from regular budgeting?

Zero-based budgeting requires you to assign every dollar of income to specific categories before the month begins, ensuring your income minus expenses equals zero. Unlike traditional budgeting that tracks spending after it happens, zero-based budgeting makes you justify every expense upfront. Regular budgets often build on previous months' spending patterns, while zero-based budgeting starts fresh each month, eliminating wasteful spending habits that might otherwise continue unchecked.

How long does it take to create your first zero-based budget?

Expect to invest 3-4 hours creating your initial zero-based budget, including time to gather financial information, list all expense categories, and make necessary adjustments to reach zero. However, once you establish your system and categories, monthly budget updates typically require only 20-30 minutes. The upfront time investment pays dividends in long-term financial clarity and control.

Can zero-based budgeting work effectively with irregular income?

Absolutely! Zero-based budgeting actually excels with variable income streams. Use your lowest typical monthly income as your baseline budget, covering all essential expenses. When higher-income months occur, allocate extra money according to predetermined priorities: emergency fund, debt payments, savings goals, then discretionary spending. This approach provides stability during lean periods while maximizing progress during abundant months.

What should I do when my zero-based budget won't balance?

When expenses exceed income in your zero-based budget, you have two primary options: reduce expenses or increase income. Start by examining variable expenses for potential cuts—dining out, entertainment, and subscription services often offer immediate savings opportunities. For income increases, consider overtime work, freelance opportunities, or selling unused possessions. Most successful budgeters combine both approaches for faster results.

How much money should I allocate to emergency funds in zero-based budgeting?

Start with an initial emergency fund goal of $1,000, treating monthly contributions as essential expenses in your zero-based budget. Once you reach $1,000, work toward 3-6 months of living expenses (or 6-8 months if you have irregular income). Calculate your monthly emergency fund contribution by dividing your target amount by your desired timeline—for example, $2,000 remaining goal ÷ 10 months = $200 monthly allocation.

Is zero-based budgeting too restrictive for maintaining quality of life?

Zero-based budgeting emphasizes intentionality, not deprivation. You can absolutely budget for entertainment, dining out, hobbies, and other enjoyable activities—you simply plan for them in advance rather than spending impulsively. Many people discover they actually spend more on meaningful experiences because they've budgeted for them guilt-free, while eliminating wasteful spending on things they don't truly value.

Which zero-based budgeting app works best for beginners?

YNAB (You Need A Budget) offers the most comprehensive zero-based budgeting features but requires a learning curve and monthly subscription fee. EveryDollar provides a simpler, free option that works well for beginners, especially those following Dave Ramsey's financial principles. For maximum control and customization, a simple spreadsheet can be incredibly effective and costs nothing beyond your time investment.

How do I handle overspending in specific categories within my zero-based budget?

When you overspend in any category, you must immediately move money from another category to cover the difference before the month ends. This forced trade-off decision makes you consciously choose between competing priorities, preventing small overages from derailing your entire budget. Review your spending patterns after several months to adjust category allocations based on actual needs rather than initial estimates.

Your Feedback Informs Our Service

There are no reviews yet. Be the first one to write one.