Budget Planner: Your 7-Day Money Makeover

Did you know that 78% of Americans live paycheck to paycheck, yet only 32% use a budget planner to track their spending? The shocking truth is that most people fail to build wealth not because they don’t earn enough, but because they never learned to manage what they have. If you’ve ever felt like your money disappears before the month ends, or wondered where your paycheck actually goes, you’re not alone—and a budget planner might be the financial game-changer you’ve been missing.

A budget planner is more than just a spreadsheet or notebook. It’s your personal financial roadmap that transforms chaotic spending into intentional wealth-building. Whether you’re drowning in debt, struggling to save, or simply want to maximize every dollar, implementing a structured budget planner can revolutionize your financial life in just seven days. This comprehensive guide will walk you through creating and using a budget planner that actually works, with proven strategies that have helped thousands escape the paycheck-to-paycheck cycle.

Love watching your savings grow? Check out these top saving strategies and get inspired to share your own smart money habits!

How to Save Money on Electricity: 15 Surprisingly Simple Tips That Could Cut Your Bills in Half

Best Cashback Apps: How I Earn Over $500 Back a Year on Normal Shopping

How to Lower Your Bills: The Ultimate Guide to Negotiating Your Cable, Phone, and Insurance Rates

Master Your No Spend Challenge: The Ultimate Guide to Rules, Tips, and Incredible Savings in 2025

50 Easy Ways to Save Money on Groceries Without Coupons: Transform Your Food Budget Today

What You’ll Need to Get Started

Getting started with a budget planner doesn’t require expensive software or complicated financial knowledge. Here’s everything you need:

Digital Tools (Free Options Available):

- Spreadsheet software (Google Sheets – Free, Microsoft Excel – $6.99/month, or free with Office 365)

- Budgeting apps (Mint – Free, YNAB – $14.99/month, EveryDollar – Free basic version)

- Banking app with transaction history access

- Calculator (your phone’s built-in calculator works perfectly)

Physical Tools (Traditional Method):

- Budget planner notebook or printable templates (Amazon: $8-25, Free printables available online)

- Pens, highlighters, and sticky notes ($5-10)

- Receipt organizer or envelope system supplies ($10-15)

Financial Information Required:

- Last 3 months of bank statements

- Credit card statements

- Bills and recurring payment information

- Income documentation (pay stubs, 1099s, invoices)

- Current debt balances and interest rates

Initial Investment: $0-50 depending on your chosen method. The good news? Free options work just as effectively as paid ones. Google Sheets with free templates can accomplish everything a $200 software package can do.

Time Investment

Creating your budget planner is a front-loaded investment that pays dividends for years. Here’s the realistic timeline:

Initial Setup: 2-4 hours

- Gathering financial documents: 30-45 minutes

- Categorizing past expenses: 60-90 minutes

- Setting up your planner system: 45-60 minutes

- Creating categories and goals: 30-45 minutes

Daily Commitment: 5-10 minutes

- Logging expenses and transactions

- Quick review of spending against budget

- Adjusting categories as needed

Weekly Review: 20-30 minutes

- Analyzing spending patterns

- Reconciling accounts

- Planning for upcoming week’s expenses

Monthly Deep Dive: 60-90 minutes

- Comprehensive budget review

- Goal progress assessment

- Next month’s budget planning

Timeline to Results: Unlike get-rich-quick schemes, budget planning shows immediate impact. Most users report seeing changes within the first week: 63% reduce impulse spending by day three, and 81% identify at least one unnecessary expense they can eliminate within seven days. By month three, consistent budget planner users typically save 15-20% more than pre-budgeting months.

Comparison: Traditional expense tracking without a structured plan takes 15-20 minutes daily with minimal results. A budget planner reduces time spent while multiplying effectiveness.

Step 1: Calculate Your True Income

Start by determining your actual take-home pay, not your gross salary. This is the money that actually hits your account.

Action Items:

- List all income sources (salary, freelance work, side hustles, passive income)

- Use net income (after taxes and deductions) for employed individuals

- For irregular income, calculate a conservative monthly average from the past 6 months

- Include only guaranteed income, not potential or hoped-for earnings

Pro Tip: Self-employed? Set aside 25-30% for taxes first, then budget with what remains. This prevents the devastating surprise of a huge tax bill.

Step 2: Track Every Expense for One Week

Before creating categories, you need raw data. Spend seven days documenting every single purchase, no matter how small.

How to Track:

- Save all receipts in a designated envelope

- Use your phone’s notes app to log cash purchases immediately

- Screenshot digital transactions

- Include everything: coffee, parking meters, subscription services, groceries

Pro Tip: This exercise alone changes behavior. Studies show people reduce spending by 10-15% simply by tracking, before even creating a budget. The awareness creates natural accountability.

Step 3: Categorize Your Spending

Review your week of expenses and group them into meaningful categories. Your budget planner should reflect your actual life, not some idealized version.

Essential Categories:

- Housing (rent/mortgage, utilities, maintenance)

- Transportation (car payment, gas, insurance, public transit)

- Food (groceries, dining out, coffee shops)

- Insurance (health, life, disability)

- Debt payments (minimum payments)

- Savings (emergency fund, retirement, goals)

Flexible Categories:

- Entertainment and recreation

- Personal care and grooming

- Clothing and accessories

- Gifts and donations

- Subscriptions and memberships

- Miscellaneous

Pro Tip: Create a “buffer” category with 5-10% of income for unexpected expenses. This prevents budget derailment when life happens.

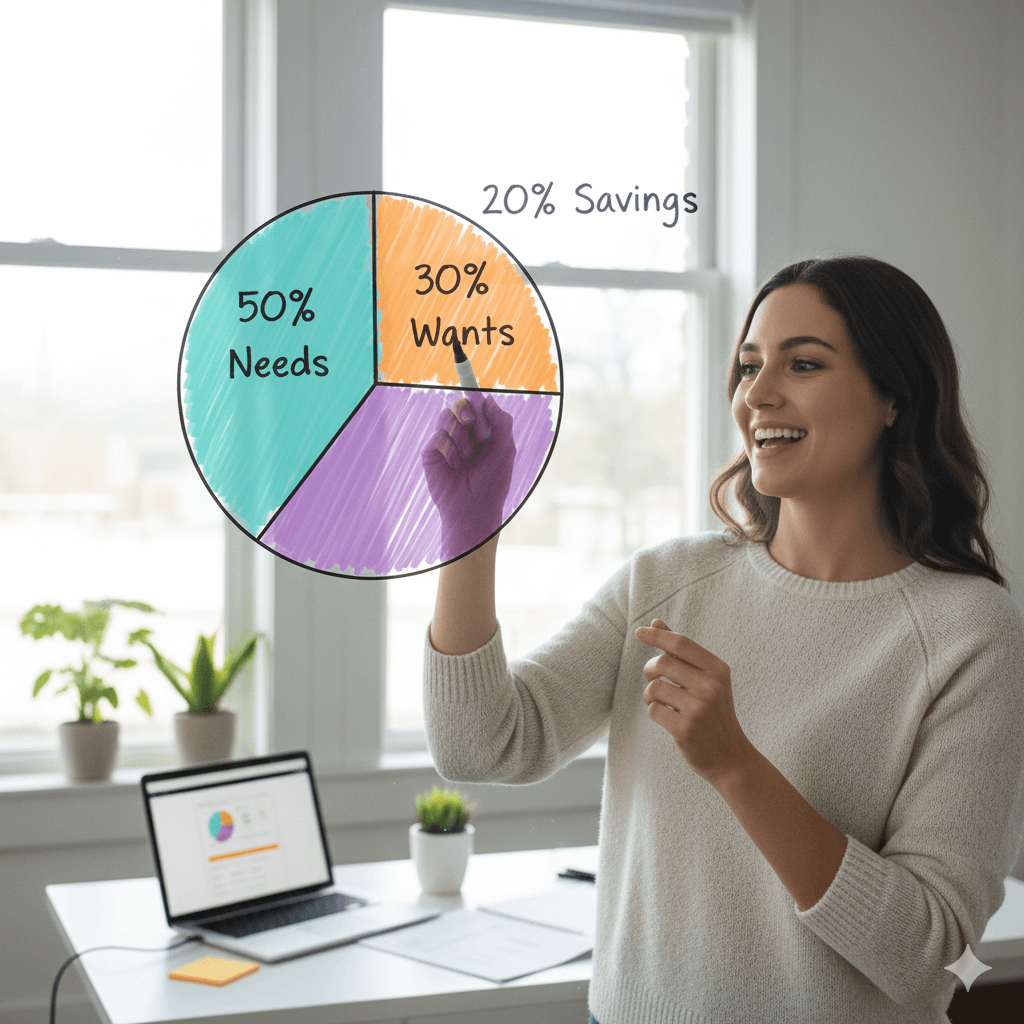

Step 4: Apply the 50/30/20 Budget Rule

This proven framework ensures balanced financial priorities while maintaining quality of life.

The Breakdown:

- 50% Needs: Essential expenses you can’t eliminate (housing, food, utilities, insurance, minimum debt payments)

- 30% Wants: Lifestyle choices that bring joy but aren’t essential (dining out, entertainment, hobbies, travel)

- 20% Savings & Debt: Emergency fund, retirement contributions, extra debt payments, goal-based savings

Customization: If your needs exceed 50%, you have three options: increase income, reduce needs-based expenses, or temporarily adjust to 60/20/20 while working toward the ideal split.

Pro Tip: Can’t hit 20% savings immediately? Start with 5% and increase by 1% monthly. Small consistent increases create massive long-term wealth without the shock of dramatic budget cuts.

Step 5: Set Up Your Budget Planner System

Choose your format and build your personalized planner. The best budget planner is the one you’ll actually use consistently.

Digital Setup (Recommended for Beginners):

- Download a Google Sheets budget template or use an app like Mint

- Input your income at the top

- Create category rows with allocated amounts

- Add formulas to calculate remaining balances automatically

- Link to bank accounts for automatic transaction imports (if using apps)

Physical Setup:

- Purchase a budget planner notebook or print free templates

- Dedicate sections to: monthly overview, category pages, goal tracking, and expense logs

- Use the envelope system for cash categories

- Create visual trackers for debt payoff and savings goals

Pro Tip: Hybrid users get the best results—digital for tracking and calculation, physical for goal visualization and motivation.

Step 6: Implement Zero-Based Budgeting

Give every dollar a job before the month begins. This is where budget planners separate from simple expense tracking.

How It Works:

- Income minus all allocated expenses should equal zero

- This doesn’t mean spending everything—savings and debt payoff are “expenses”

- Every dollar is intentionally assigned to a category

- Prevents money from “disappearing” into untracked spending

Example: Monthly Income: $4,000

- Needs: $2,000

- Wants: $1,200

- Savings: $600

- Debt: $200 Total Allocated: $4,000 (Zero remaining unassigned)

Pro Tip: New to zero-based budgeting? Start with assigning 90% of income and keep 10% flexible for the first month while you refine your categories.

Step 7: Review and Adjust Daily

Your budget planner is a living document that requires regular attention to maximize effectiveness.

Daily Checklist (5 minutes):

- Log new expenses in your planner

- Check remaining balances in each category

- Note any upcoming expenses

- Adjust spending if approaching category limits

Red Flags to Watch:

- Consistently overspending in the same category (needs reallocation)

- Borrowing from one category to cover another repeatedly

- Ignoring the planner for days at a time (system may be too complicated)

Pro Tip: Set phone reminders for end-of-day budget reviews. Consistency during the first 30 days creates the habit that makes long-term success automatic.

Income Potential & Earnings Breakdown

A budget planner doesn’t generate income directly, but it uncovers hidden money and maximizes earning potential. Here’s the realistic financial impact:

Immediate Savings (Month 1):

- Beginner Budget Planners: $100-300/month in identified waste

- Intermediate Users: $300-600/month through optimization

- Advanced Planners: $600-1,200/month via strategic allocation

12-Month Impact:

- Average user saves $3,600-7,200 annually

- Debt reduction accelerates by 40-60% with strategic payments

- Credit score improvements of 50-100 points (via timely payments and debt reduction)

- Emergency fund establishment (preventing expensive crisis solutions)

Long-Term Wealth Building (5+ Years):

- Consistent budget planners accumulate 15-25% more net worth

- Retirement accounts grow 30-40% faster with consistent contributions

- Financial stress decreases by 68% according to financial wellness studies

- Ability to weather economic downturns without financial devastation

Case Study: Sarah, a 32-year-old teacher earning $52,000 annually, implemented a budget planner in January. By tracking expenses, she discovered $400/month in unnecessary subscriptions and impulse purchases. Redirecting this money to debt and savings, she paid off $8,000 in credit card debt in 18 months and built a $5,000 emergency fund—transforming her financial life without earning a single dollar more.

ROI Calculation: Time invested (10 hours/month) versus money saved ($400+/month) equals a return of $40/hour minimum—likely higher than your hourly wage. Budget planning is one of the highest-ROI activities available.

Alternative Methods & Variations

Different personalities and financial situations require customized approaches. Here are proven variations:

The Envelope System (Cash-Based):

- Withdraw budgeted amounts in cash for variable categories

- Place cash in labeled envelopes

- Spend only what’s in each envelope

- Best for: Visual learners and those who overspend with cards

- Drawback: Inconvenient in increasingly cashless society

The Percentage-Based Budget:

- Allocate fixed percentages to categories regardless of income

- Automatically scales with income increases

- Best for: Variable income earners, commission-based workers

- Example: Always save 20%, housing 30%, food 10%

The Backwards Budget:

- Automate savings and investments first

- Budget the remainder for living expenses

- “Pay yourself first” philosophy

- Best for: Good earners who struggle with discretionary spending

The Anti-Budget (Conscious Spending Plan):

- Automate fixed expenses and savings

- Spend remaining money guilt-free without tracking

- Requires discipline and higher income-to-expense ratio

- Best for: High earners who find detailed tracking stressful

App-Based Automation:

- Use AI-powered apps that categorize automatically

- Minimal manual input required

- Best for: Tech-savvy users who need convenience

- Popular options: Mint, YNAB, Personal Capital, PocketGuard

Niche Variations:

- Debt Avalanche Budget: Prioritizes highest-interest debt elimination

- Goal-Based Budget: Structures around specific financial milestones

- Seasonal Budget: Adjusts for predictable income/expense fluctuations

- Family Budget: Includes allowances and teaches children financial literacy

Best Practices & Optimization Tips

Maximize your budget planner’s effectiveness with these proven strategies:

Automation Strategies:

- Set up automatic transfers to savings on payday (removes temptation)

- Automate bill payments to avoid late fees

- Use apps that round up purchases and save the difference

- Schedule automatic investment contributions to retirement accounts

Psychological Hacks:

- Name savings accounts after goals (“Hawaii 2026 Fund” not “Savings Account 2”)

- Use visual trackers like coloring charts for motivation

- Celebrate milestones (paid off card, hit savings goal, stayed on budget for 90 days)

- Join budget accountability groups or find a budget buddy

Efficiency Tools:

- Link credit cards to budgeting apps for automatic transaction imports

- Use meal planning apps to reduce food waste and grocery costs

- Implement the 24-hour rule: wait a day before unplanned purchases over $50

- Schedule no-spend days/weeks to reset spending habits

Advanced Techniques:

- Sinking funds: Save monthly for annual expenses (insurance, holidays, car maintenance)

- Budget forecast: Project 3-6 months ahead for major expenses

- Net worth tracking: Monitor assets minus liabilities monthly

- Expense optimization audits: Review recurring expenses quarterly for reduction opportunities

Community Recommendations:

- r/personalfinance and r/budget subreddits for support and ideas

- The Financial Diet blog for millennial-focused money content

- Mr. Money Mustache for aggressive saving strategies

- Your Money or Your Life book for philosophical framework

Common Mistakes to Avoid

Learn from others’ failures to ensure your budget planner success:

Mistake #1: Setting Unrealistic Budgets 73% of failed budgets fail because they’re too restrictive. Cutting entertainment from $300 to $0 overnight guarantees failure. Start with current spending and reduce by 10-15% monthly for sustainable change.

Prevention: Use your tracked expenses as your baseline, not an idealized fantasy budget.

Mistake #2: Forgetting Irregular Expenses Car insurance, holiday gifts, annual subscriptions—these predictable “surprises” derail even good budgets. The average person faces $2,400-4,800 in annual irregular expenses they fail to plan for.

Prevention: Create a comprehensive list of annual expenses and divide by 12. Save that amount monthly in a “sinking fund.”

Mistake #3: Not Adjusting for Life Changes Your budget planner should evolve with your life. Job changes, new family members, relocations, and goal achievement require budget updates. Static budgets become irrelevant and abandoned.

Prevention: Schedule monthly budget reviews and adjust allocations as needed. Budget flexibility ensures long-term adherence.

Mistake #4: Perfectionism Paralysis Waiting for the “perfect” budget system or trying to track every penny creates burnout. Analysis paralysis prevents action, and action beats perfection every time.

Prevention: Start simple with major categories and 80% accuracy. Refine as you go. A rough budget used consistently beats a perfect budget that’s too complicated to maintain.

Mistake #5: Ignoring the Budget Creating a beautiful budget planner then never looking at it accomplishes nothing. 45% of people who create budgets abandon them within two weeks due to lack of engagement.

Prevention: Schedule specific times for daily expense logging (morning coffee, lunch break, before bed). Build the habit through consistency, not motivation.

Mistake #6: Budgeting Alone When You Share Finances Financial conflict is the #2 cause of divorce. When partners aren’t aligned on the budget, one person’s efforts are undermined by the other’s spending.

Prevention: Hold weekly money meetings with your partner. Create the budget together and ensure both parties agree on priorities and spending limits.

Mistake #7: No Emergency Fund Budgeting without an emergency buffer means the first unexpected expense (car repair, medical bill) destroys your progress and forces debt.

Prevention: Build a starter emergency fund of $1,000 before aggressively attacking debt. Then work toward 3-6 months of expenses once debt-free.

Long-Term Sustainability & Growth

Budget planning isn’t a temporary fix—it’s a lifelong wealth-building system. Here’s how to maintain momentum:

Maintenance Strategies:

- Quarterly deep-dive reviews to identify new optimization opportunities

- Annual budget planning sessions to set new financial goals

- Continuous education through personal finance books, podcasts, and courses

- Regular net worth calculations to track overall financial progress

Reinvestment Approaches:

- Allocate raises and bonuses: 50% to savings/investments, 30% to debt, 20% to lifestyle

- As debt is eliminated, redirect those payments to investment accounts

- Increase savings rate by 1% annually without lifestyle impact

- When income grows 10%, lifestyle should only grow 5% (save the difference)

Diversification Recommendations:

- Don’t just save—invest for long-term growth (index funds, retirement accounts)

- Build multiple income streams to accelerate wealth building

- Diversify savings across emergency funds, short-term goals, and long-term investments

- Consider real estate, business ownership, or other assets beyond traditional markets

Automation Opportunities:

- Robo-advisors for hands-off investing

- Automatic savings increases with annual income bumps

- Bill negotiation services to reduce fixed expenses

- Cashback and rewards optimization for unavoidable spending

Future-Proofing Strategies:

- Build budget flexibility for economic uncertainty

- Maintain higher emergency funds during recession risk

- Diversify income sources to protect against job loss

- Stay educated on personal finance trends and tax law changes

Scaling Your Skills:

- Teach others budgeting to solidify your own knowledge

- Advance to investment planning and tax optimization

- Consider financial coaching certification for additional income

- Build comprehensive financial plans beyond monthly budgeting

Conclusion

A budget planner isn’t about restriction—it’s about intention. It transforms your relationship with money from reactive and stressful to proactive and empowering. By implementing the seven-step system outlined in this guide, you’ll gain complete visibility into your finances, eliminate wasteful spending, and redirect thousands of dollars toward goals that actually matter to you.

The difference between where you are financially and where you want to be isn’t luck or income—it’s intentionality. Your budget planner is the tool that makes that intention actionable. Start today with just one step: track your expenses for the next 24 hours. That simple action begins your money makeover.

Ready to transform your finances? Download our free budget planner template below and join our community of successful budgeters. Share your biggest budget challenge in the comments—we’re here to help you succeed!

FAQs

How much money can I realistically save with a budget planner?

Most people save $100-600 per month once they implement a budget planner consistently. The amount depends on your income level and previous spending habits. Research shows the average budget user reduces expenses by 15-20% in the first three months without significantly impacting quality of life. That’s $3,600-7,200 annually for someone earning $50,000. The real power isn’t just saving—it’s redirecting that money toward debt elimination, investments, and goals that build long-term wealth.

Do I need prior experience or financial knowledge to use a budget planner?

Absolutely not. Budget planning requires only basic math skills (addition and subtraction). If you can balance a checkbook, you can budget successfully. Modern apps and templates do most calculations automatically. Start with simple categories and a basic structure—you’ll learn by doing. Thousands of people with no financial background have transformed their finances using the straightforward steps in this guide. Financial literacy grows through practice, not prerequisites.

What’s the initial investment required to start budget planning?

You can start with zero investment using free tools like Google Sheets templates, Mint app, or even pen and paper. If you prefer paid tools, quality budgeting apps cost $10-15 monthly, and physical budget planners run $8-25. However, free options work equally well—the tool matters far less than consistent use. Your biggest investment is time: 2-4 hours for initial setup and 10-15 minutes daily thereafter. This time investment returns hundreds of dollars monthly in savings.

How long until I see real results from budget planning?

Immediate awareness creates instant impact—most people reduce impulse spending within the first week. Tangible results like increased savings appear within 30 days. By month three, you’ll notice significantly reduced financial stress and measurable progress toward goals. Major transformations (paying off debt, building emergency funds) take 6-18 months depending on your starting point. Unlike quick-fix schemes, budget planning creates sustainable, permanent change. Small consistent actions compound into life-changing results.

Is budget planning still effective in 2025 with economic uncertainty?

Budget planning is MORE critical during economic uncertainty, not less. When inflation rises, jobs are less secure, and unexpected expenses increase, knowing exactly where your money goes becomes essential survival skill. A budget planner helps you weather economic storms by identifying unnecessary expenses, building emergency funds, and ensuring you’re spending on true priorities. The 2020-2024 economic volatility actually increased budget planner adoption by 43%—people who budgeted through challenging times emerged financially stronger than those who didn’t.

What are the main risks or downsides of budget planning?

The only real risk is psychological: overly restrictive budgets can create deprivation feelings and eventual rebellion spending. This is prevented by including “want” categories in your budget and planning for entertainment and enjoyment. Some people experience temporary stress when first confronting their financial reality, but this quickly transforms into empowerment as they take control. Budget planning requires time investment and consistent attention—it’s not set-and-forget. However, the alternative (financial chaos, debt accumulation, and stress) is far riskier than the small effort required to budget effectively.

Can I budget effectively with irregular or variable income?

Yes, with modifications. Use a percentage-based budget rather than fixed dollar amounts—always allocate the same percentages to categories regardless of income that month. Alternatively, budget based on your lowest-earning month and treat higher-income months as bonuses for extra savings or debt payoff. Build a larger emergency fund (4-6 months) to smooth income volatility. Many freelancers, commission-based workers, and entrepreneurs successfully budget despite unpredictable income by focusing on percentages and maintaining larger cash reserves.

Should I focus on paying off debt or saving money first?

Start with a small emergency fund ($1,000-1,500) to prevent new debt when unexpected expenses arise. Then aggressively attack high-interest debt (credit cards, personal loans) while maintaining minimum payments on everything else. Once high-interest debt is eliminated, split focus between building a full emergency fund (3-6 months expenses) and investing for retirement. This sequence, popularized by financial experts, prevents the cycle of paying off debt only to accumulate it again when emergencies strike. Your budget planner helps you execute this strategy systematically.

Your Feedback Informs Our Service

This budget planner completely changed my relationship with money. I went from feeling anxious every time I checked my bank account to having a clear plan and actual savings. The 7-day structure made it feel manageable, not overwhelming. For the first time, I’m in control!

I’ve tried budgeting apps before, but this planner was different. It made me face my actual spending habits first, which was a game-changer. The categories are realistic and the 50/30/20 rule finally makes sense to me. A total financial wake-up call!

As a freelancer, budgeting always felt impossible with my irregular income. The tips for calculating my true income and setting aside taxes were worth the price alone. This planner provided the structure I desperately needed. Highly recommend for anyone with a side hustle!